We all dream of our children having an amazing future, getting into the best schools, maybe studying abroad, and definitely having the freedom to chase their true calling. But honestly, when it comes to paying for that education, good intentions alone won’t cut it.

Education costs in India and abroad have been rising faster than general inflation for years. Professional courses, private universities, overseas education, skill-based programs — they all come with price tags that grow, year after year. What feels affordable today may feel overwhelming ten years later.

This is where early planning changes the story.

Systematic Investment Plans (SIPs) embody discipline, structure, and consistency — qualities essential to effective parenting. Starting your SIPs early grants your investment the most powerful benefit: time.

This blog explains how parents can start SIPs for their child’s education, how to structure them sensibly, and how to stay on track despite life’s many distractions.

Why Child Education Planning Cannot Be Delayed

Education is not a one-time expense. It is a long journey with multiple milestones — primary school, higher secondary, undergraduate studies, and possibly post-graduation or overseas education. Each stage brings a higher financial commitment.

Indian families are really getting caught in a serious “education debt trap” right now, in early 2026. Private school costs are skyrocketing, way faster than general inflation. Sure, the official education inflation for 2025 was only about 3.3% to 4.1%, but honestly, over 80% of parents are seeing fee hikes over 10% annually. Plus, a lot of schools are even giving a heads-up about big “step-up” increases coming. It’s not helping that everyone’s switching to super-expensive IB boards (up to ₹15 lakh a year!) just to get that global stamp of approval. And get this: schools are even justifying huge fee jumps with vague charges for “AI/tech levies.”

Education is now a “must-pay” expense that’s eating up a huge chunk of family savings, forcing people to redirect funds to non-negotiable tuition and all the other associated costs. Many parents assume they have “enough time” and plan to fund education using future income, bonuses, or asset sales. The risk here is unpredictability. Careers change. Businesses slow down. Health expenses appear unannounced. Planning early does not mean locking money away blindly. It means creating a structured path so future choices remain options instead of compromises.

Why SIPs Work Well for Education Goals

SIPs work because they align with how real life operates.

Income and expenses happen monthly, and SIPs fit that rhythm perfectly. Instead of finding the right time to invest or waiting for a big chunk of cash, SIPs let you participate consistently over time.

For long-term goals like education, SIPs offer three key advantages:

SIPs:

- Reduce timing risk: Gradual investing spreads market entry, minimizing short-term volatility impact.

- Create financial discipline: Automation removes emotion, curbing the urge to pause investments.

- Harness compounding: Regular contributions grow significantly over time when undisturbed.

The Earlier You Start, the Less You Strain

A simple truth often gets ignored: starting early reduces pressure later.

When parents begin investing during their child’s early years, the monthly investment amount required is significantly lower than when planning starts late. Time absorbs much of the burden.

Starting early also allows flexibility. If income rises, SIPs can be increased. If expenses spike temporarily, contributions can be adjusted without derailing the entire plan.

Late starters, on the other hand, often face uncomfortable trade-offs — higher monthly commitments, increased risk-taking, or last-minute borrowing.

Planning early is not about predicting the future perfectly. It is about keeping options open.

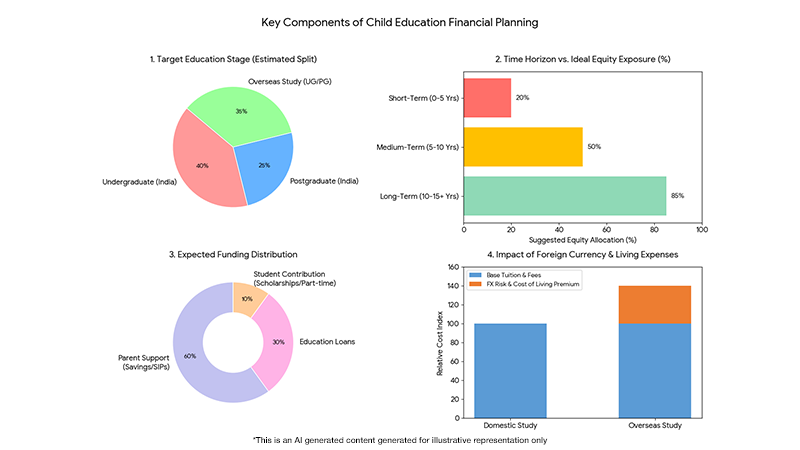

Step 1: Define the Education Goal Clearly

Before starting any SIP, clarity is essential.

Education planning should begin with broad assumptions, not rigid certainty. Parents do not need to know the exact college or course today, but they should estimate:

– The likely stage of education being planned for (undergraduate, postgraduate, overseas study)

– The expected time horizon

– Whether the education may involve foreign currency expenses

– How much support the parent intends to provide versus student contribution or loans

These assumptions help shape the investment horizon and risk approach. The goal is preparedness.

As the child grows and preferences become clearer, the plan can evolve.

Step 2: Match Time Horizon with Risk Thoughtfully

Time horizon plays a critical role in how education SIPs should be structured.

For goals that are more than ten years away, investments typically have more time to ride market cycles. Short-term fluctuations matter less when the horizon is long. As the goal gets closer, it’s smarter to focus on protecting and growing what you’ve saved rather than trying to chase high growth. Slowly reducing risk helps keep your hard-earned savings safe.

This shift doesn’t happen overnight. It happens through regular evaluation and adjustment of the investments—a process a lot of investors forget about.

Education planning should mature as your child does.

Step 3: Decide the SIP Amount Realistically

The best SIP is one that continues uninterrupted.

Parents often make the mistake of starting with aggressive amounts that feel impressive but become difficult to sustain. Consistency beats ambition.

A realistic SIP amount should consider current income, essential household expenses, existing financial commitments, and future responsibilities such as housing or retirement.

SIPs can always be stepped up gradually as income grows. Starting smaller and increasing later is far more effective than starting big and stopping altogether.

Stability is the strategy.

Step 4 : Build in Flexibility

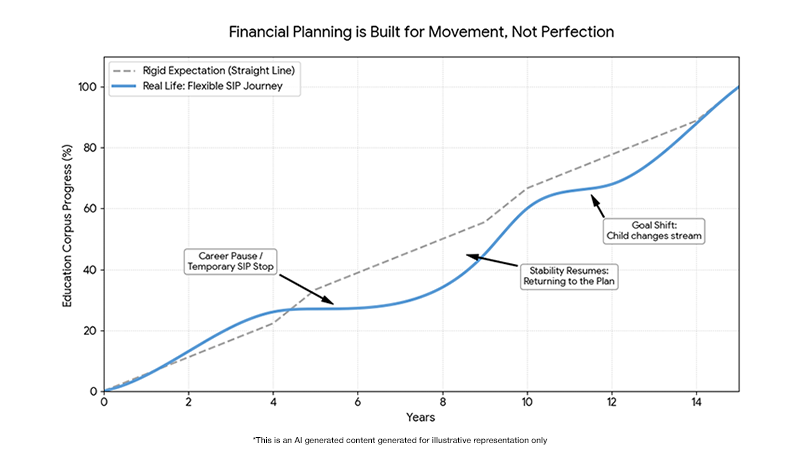

Many factors such as career pauses, business cycles, and evolving family responsibilities remind us that life doesn’t move in straight lines. Income changes. Priorities shift. What feels certain today can look very different a few years down the line.

That’s why financial planning works best when it’s built for movement—not perfection. Plans must breathe, adapt, and stay relevant as real life unfolds.

Education SIPs should be structured with flexibility in mind. Temporary pauses or adjustments should not feel like failure. What matters is returning to the plan once stability resumes.

Flexibility also applies to goals. A child’s interests may change. Study locations may shift. Planning frameworks should allow adaptation without financial shock. A good plan bends without breaking.

We’ve actually talked about the benefits of mutual funds beside SIP in a lot of detail in our article, “Things You Didn’t Know Mutual Funds Could Do (But They Can),” which gives you more options to choose from.

Staying on Track: The Real Challenge

Starting SIPs is easy. Staying invested for fifteen or twenty years is the real work.

Markets will fluctuate. News will distract. Advice from family, relatives & friends will confuse. During downturns, fear often whispers that stopping investments is the safe move.

Ironically, long-term goals benefit most from consistency during volatile periods. Discipline during uncertainty is what separates intention from outcome.

Regular reviews help. Annual check-ins allow parents to adjust assumptions, increase contributions if possible, and realign the plan with evolving goals.

Education planning is not about reacting to headlines. It is about responding to life stages.

As highlighted in “Why Pausing Your SIP During Market Lows Is the Worst Move An Investor Can Make,” staying invested during difficult market phases is especially important for long-term goals like a child’s education.

An Example

The earlier you start, the less you need to invest monthly to achieve your goal.

- Starting a SIP of ₹10,000 per month for 15 years with a long-term assumed return of around 12% can help build a corpus close to ₹50 lakh.

- If the same goal of 50 lakhs is delayed by 5 years, the required monthly investment may rise to around ₹22,000, increasing the financial strain significantly.

The difference here is not returns — it is time.

Planning for College Education

Suppose your child is 5 years old, and you anticipate needing ₹35 lakh for their college education in 13 years.

Here’s how:

- If you invest ₹10,000 monthly in an equity mutual fund with an average return of 12%, you can achieve this goal.

By starting now, you leverage the power of compounding and avoid the pressure of arranging a lump sum at the last moment.

Common Mistakes Parents Make

Many parents unknowingly undermine their own plans.

- Delaying the start by waiting for perfect clarity, which often never comes.

- Investing without linking the SIPs to a specific goal, making it easier to divert funds later.

- Ignoring inflation by planning with today’s costs instead of future realities, leading to significant shortfalls.

- Forgetting to balance education planning with the parents’ own financial security, such as retirement stability.

A strong plan considers the whole family, not just one milestone.

The Emotional Side of Education Planning

Education planning is deeply emotional.

Parents want to give their children freedom. They want to avoid burdening them with debt. They want choices to remain open.

Ironically, emotional decision-making often leads to reactive financial behaviour. Structured planning helps keep emotions in check by creating a roadmap that absorbs uncertainty.

A calm plan today reduces anxiety tomorrow.

How SubhShanti Wealth Supports Child Education Planning

At SubhShanti Wealth, child education planning begins with conversation rather than just recommending products. We assist families in structuring their financial journey responsibly, with clarity and discipline. Education planning is approached as part of a broader financial picture.

- Clarifying education goals: We assist parents in articulating realistic education objectives, estimate future costs conservatively, and align investment time horizons accordingly—keeping the focus on process, suitability, and long-term consistency rather than short-term outcomes.

- Ongoing reviews and course correction: Regular reviews form a critical part of the journey. As income changes, family responsibilities evolve, or education paths become clearer, we help adjust the structure calmly and methodically, without emotional disruption.

- Balancing competing priorities: We ensure education planning works in harmony with other financial needs such as emergency funds and retirement planning, so one goal does not come at the cost of another.

After sorting out the education planning, getting a house usually becomes the next big financial goal for most families. We’ve actually talked about this before on our blog, “How Mutual Funds Can Make Home Buying Easy.” It really shows how flexible SIPs can be.

Discipline Is the Real Gift

Education is one of the most meaningful gifts a parent can offer. But the manner in which it is funded matters just as much as the funding itself.

Starting SIPs early teaches patience. Staying invested teaches discipline. Reviewing periodically teaches responsibility.

These qualities don’t just build a corpus. They build confidence — for parents and children alike.

When education planning is done thoughtfully, money becomes an enabler.

A Long-Term Perspective

Child education planning is a marathon. It rewards early action, steady commitment, and thoughtful review.

SIPs are not a guarantee of outcomes. They are a framework for participation. When combined with time, discipline, and realistic expectations, they become a powerful planning tool.

The future will always carry uncertainty. Planning early reduces regret.

In the end, the goal is simple: when the time comes, finances should support choices, not limit them.

That is the quiet power of starting early & staying the course.

Disclaimer

This article is intended solely for educational and informational purposes. It does not constitute investment advice, trading recommendations, or a solicitation to buy or sell any securities or financial instruments. The views expressed are based on publicly available data, regulatory studies, and industry observations, including reports published by the Securities and Exchange Board of India (SEBI). Readers are advised to assess their financial objectives, risk appetite, and suitability before making any investment or trading decisions. Derivatives trading, including Futures & Options (F&O), involves substantial risk and may not be suitable for all investors. Past performance is not indicative of future results. Investors should consult a SEBI-registered investment adviser or other qualified financial professional before acting on any information presented herein.