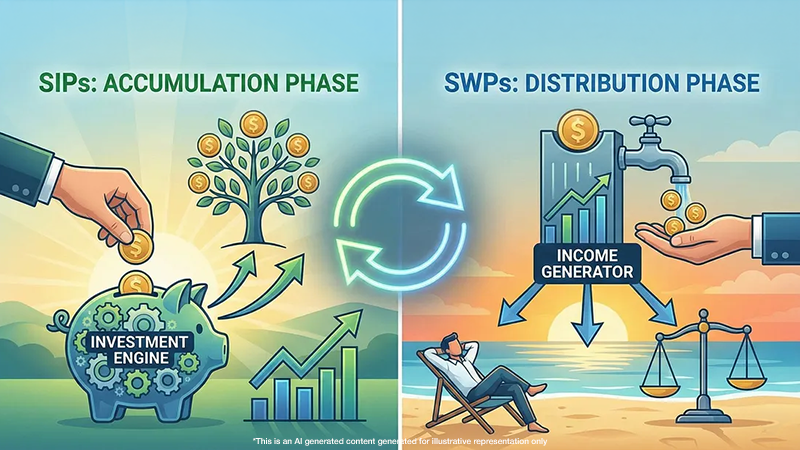

Retirement planning doesn’t end the day you stop earning. That’s merely the handover—from accumulation to distribution. If SIPs are the engine that builds your retirement corpus, a Systematic Withdrawal Plan (SWP) is the transmission that converts that accumulated power into steady, usable income.

In India, this transition is often poorly managed. Many retirees either withdraw lump sums too early or rely excessively on fixed deposits that struggle to keep up with inflation. The result is familiar: anxiety about longevity, fear of running out of money, and portfolios that grow conservative too soon.

SWPs exist to solve precisely this problem.

What Is an SWP — Explained Simply

A Systematic Withdrawal Plan (SWP) allows you to withdraw a fixed amount at regular intervals—monthly, quarterly, or annually—from your mutual fund investments.

Instead of liquidating your entire corpus at once, you redeem units gradually. The remaining money stays invested and continues to participate in market growth.

Think of it as creating your own pension, but with three crucial upgrades:

- Flexibility (you control amount and frequency)

- Growth potential (unlike fixed pensions)

- Tax efficiency (when structured well)

Why SWPs Matter in Retirement

Retirement today can easily last 20–30 years. During this phase, two risks dominate everything else.

1. Longevity Risk

Outliving your money is a far bigger threat than short-term market volatility. SWPs reduce this risk by pacing withdrawals and keeping part of the corpus growing.

2. Inflation Risk

Expenses, especially healthcare, don’t freeze after retirement. They rise. SWPs help counter inflation by maintaining equity or hybrid exposure even after retirement.

In short, SWPs are not about squeezing returns. They’re about making money last.

How SWPs Work in Practice

Here’s the mechanics, without jargon.

- You choose a mutual fund (often hybrid or debt-oriented post-retirement).

- You decide the withdrawal amount and frequency.

- On each withdrawal date, a small number of units are redeemed.

- The rest of the units remain invested.

If portfolio returns exceed your withdrawal rate, the corpus can sustain itself for a very long time—sometimes even grow.

This is why SWPs are best viewed not as a product, but as a process.

SWP as a Private Pension Engine

Traditional pensions offer certainty—but little flexibility or growth. SWPs flip that equation.

| Feature | Traditional Pension | SWP |

| Control | Limited | Full control |

| Inflation protection | Weak | Strong (with equity exposure) |

| Flexibility | Fixed rules | Customisable |

| Tax efficiency | Often taxed fully | Capital-gains based |

| Legacy planning | Limited | Remaining corpus can be passed on |

In effect, SWPs allow retirees to design a personal pension system, tailored to their lifestyle and risk tolerance.

Benefits and Risks of SWPs — A Clear Comparison

| Aspect | Benefits | Risks |

| Regular income | Predictable cash flow, similar to salary | Poor fund selection can impact sustainability |

| Growth potential | Remaining corpus stays invested | Excessive withdrawals can erode capital |

| Tax efficiency | Only capital gains portion is taxed | Tax rules vary by fund type and holding period |

| Flexibility | Withdrawal amount can be adjusted | Requires discipline and periodic review |

| Longevity management | Helps money last longer | Market downturns need careful asset allocation |

The risks aren’t structural flaws. They’re design risks—solved through proper planning and periodic rebalancing.

An SWP’s longevity depends not just on how much you withdraw, but on how intelligently the remaining corpus is managed. Market cycles can distort asset allocation over time, which is why disciplined retirees rely on periodic re-alignment. Our article, Rebalancing: The Understated Discipline That Keeps Portfolios Healthy explains how this quiet discipline helps retirement income strategies remain resilient across decades.

How Much Can an SWP Deliver? (Illustrative)

Assume:

- Retirement corpus: ₹3 crore

- Withdrawal: ₹1 lakh per month (₹12 lakh annually)

- Portfolio return: ~8–9% (conservative post-retirement mix)

That’s a withdrawal rate of ~4%. Historically, such withdrawal rates—when combined with balanced portfolios—have shown high sustainability over long retirement periods.

Data from the mutual fund industry consistently shows that withdrawal rates below long-term expected returns significantly reduce the probability of corpus exhaustion.

(Industry data sources: Association of Mutual Funds in India, Securities and Exchange Board of India)

A Simple Withdrawal Strategy for Retirement

| Withdrawal Step | What to Do | Why It Matters |

| Decide annual withdrawal | Withdraw around 3.5%–4.5% of your total retirement corpus per year | Helps ensure your money lasts through a long retirement |

| Use SWP | Set up a Systematic Withdrawal Plan for monthly income | Creates a steady “salary-like” cash flow and avoids lump-sum mistakes |

| Align money to time | Keep 1–3 years of expenses in debt or liquid funds; rest in hybrid/equity | Protects monthly income from short-term market swings |

| Withdraw regularly | Take out a fixed amount monthly | Improves predictability and budgeting |

| Increase gradually | Review and raise withdrawals every 2–3 years, not annually | Prevents overspending and protects long-term sustainability |

| Review annually | Check portfolio once a year and rebalance if needed | Keeps risk aligned without emotional reactions |

| Avoid panic actions | Don’t change withdrawals during market corrections | Markets recover; rushed decisions often don’t |

In essence: a good withdrawal strategy is slow, steady, and structured—designed to support your lifestyle while letting your money quietly keep working in the background.

SWP vs Fixed Deposits: A Quiet Comparison

Fixed deposits feel safe. But safety without growth is a slow leak.

| Metric | FD | SWP |

| Returns (post-tax) | Often below inflation | Potentially inflation-beating |

| Income flexibility | Fixed | Adjustable |

| Tax treatment | Fully taxable | Capital gains-based |

| Longevity protection | Weak | Stronger |

| Wealth preservation | Low | Moderate to High |

FDs still have a role—for liquidity and stability. But relying on them alone for 20+ years of retirement income is mathematically fragile.

SIPs and SWPs: Two Halves of One Strategy

Retirement planning works best when accumulation and withdrawal are designed together.

- SIPs build the corpus through discipline, compounding, and time

- SWPs distribute the corpus through structure, control, and sustainability

If you haven’t, please refer to our detailed blog How SIP Can Fund Your Retirement, which explains how consistent investing lays the groundwork for a robust retirement corpus. Together, these two systems form a complete lifecycle approach to retirement—earning, growing, and finally using your wealth without fear.

The SubhShanti Wealth Lifecycle Made for You

SubhShanti Wealth specializes in the “Accumulation to Distribution” financial lifecycle, using a two-part strategy: SIP for building wealth and SWP for distributing it.

- 1. Accumulation (SIP): Wealth creation is a marathon. We set up disciplined, goal-based SIPs, using Rupee Cost Averaging and a Step-Up Strategy (increasing contributions annually) to reach targets like a ₹5 Crore corpus.

- 2. Transition: Once the corpus is built, we manage the critical shift by Asset Rebalancing (moving from equity to stable Hybrid funds) and Tax Optimization (utilizing LTCG exemptions).

- 3. Distribution (SWP): This phase creates a “Second Salary.” We structure an SWP for Predictable Income (fixed monthly credit) while prioritizing Capital Preservation by setting a safe Withdrawal Rate (4–6%). Unlike fixed pensions, SWP amounts can be adjusted for Inflation Protection.

Comparison: SIP vs. SWP with SubhShanti Wealth

| Feature | SIP (Phase 1) | SWP (Phase 2) |

| Direction | Money moves from Bank -> Mutual Fund | Money moves from Mutual Fund -> Bank |

| Primary Goal | Wealth Creation (The “Sowing”) | Regular Income (The “Harvesting”) |

| Benefit | Power of Compounding | Tax-efficient “Pension” |

| Duration | During your earning years | During retirement or career breaks |

The Real Role of SWPs

SWPs don’t promise excitement. They promise continuity.

They turn accumulated wealth into:

- Monthly dignity

- Financial independence

- Choice without anxiety

Retirement isn’t about extracting the maximum rupee. It’s about creating a rhythm of income that lasts as long as you do.

SIPs help you reach the mountain & help you live comfortably at the summit without rushing downhill.

Disclaimer

This article is intended solely for educational and informational purposes. It does not constitute investment advice, trading recommendations, or a solicitation to buy or sell any securities or financial instruments. The views expressed are based on publicly available data, regulatory studies, and industry observations, including reports published by the Securities and Exchange Board of India (SEBI). Readers are advised to assess their financial objectives, risk appetite, and suitability before making any investment or trading decisions. Derivatives trading, including Futures & Options (F&O), involves substantial risk and may not be suitable for all investors. Past performance is not indicative of future results. Investors should consult a SEBI-registered investment adviser or other qualified financial professional before acting on any information presented herein.