Introduction

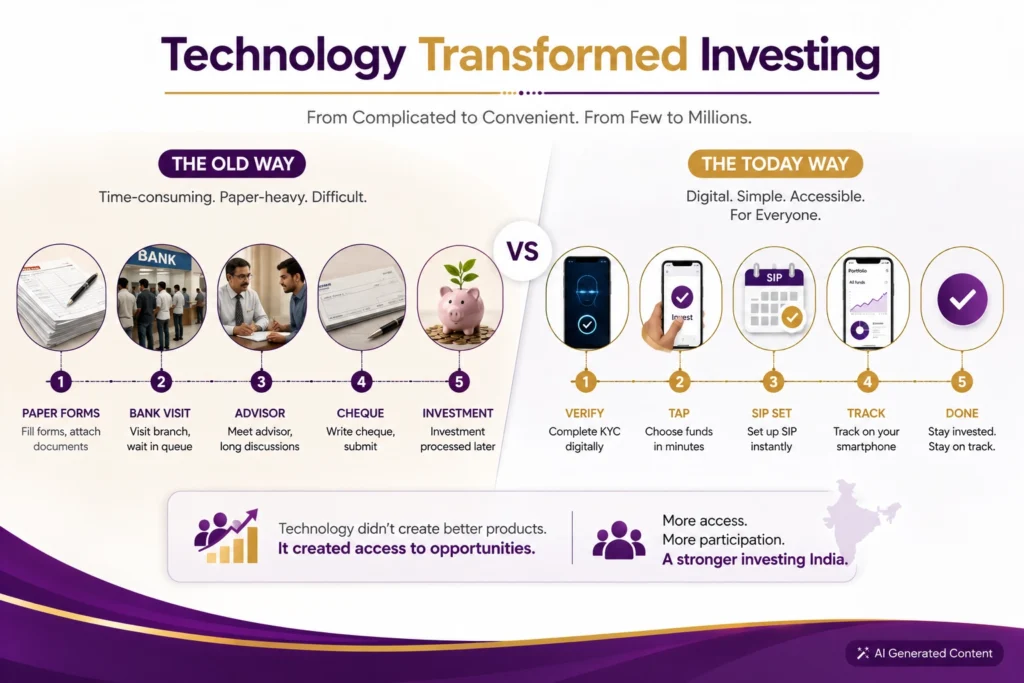

Investing behaviour has changed dramatically over the last decade, but better technology hasn’t always created better investors. Picture a young professional on her lunch break.

She opens an investment app, logs in with Face ID, reviews a few mutual funds, starts a ₹5,000 SIP, and returns to work before her coffee has cooled. The entire process takes less than five minutes. No paperwork. No personal conversation. No customization.

A decade ago, this would have seemed extraordinary. Today, it’s completely normal.

Technology has fundamentally changed the way India invests. Just as smartphones transformed how we communicate, shop, travel and consume entertainment, they have also reshaped our relationship with money. Investing, once seen as intimidating and reserved for financially savvy individuals, has become accessible to anyone with a smartphone and a bank account.

This shift is what we call the AirPod Effect.

The name isn’t really about wireless earbuds. It’s a metaphor for a generation that values speed, convenience and independence. Whether it’s ordering food, booking a holiday or learning a new skill, the expectation is simple: if technology can remove friction, why shouldn’t it?

Investing has naturally followed the same path.

Digital platforms have simplified everything from opening an account to starting a Systematic Investment Plan (SIP). According to the Association of Mutual Funds in India, SIP accounts crossed 10 crore in 2024, while monthly SIP contributions continue to scale new highs. Millions of first-time investors, including many from Tier II and Tier III cities, are participating in financial markets for the first time because technology has lowered the barriers to entry.

That deserves recognition.

For years, access was one of the biggest obstacles to investing. Financial products often felt complicated, paperwork was cumbersome, and investing was frequently associated with banks, experts and long conversations that discouraged many first-time investors.

Today, those barriers have largely disappeared.

But removing barriers raises another question.

When investing becomes as effortless as ordering a meal online, do we begin to underestimate how difficult investing actually is?

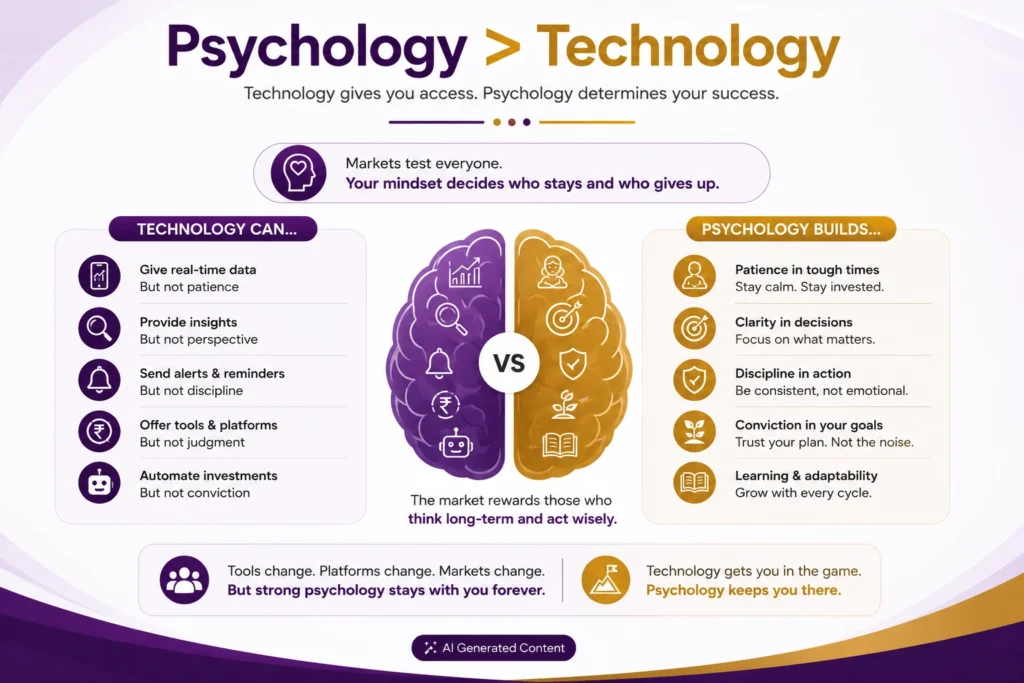

The answer matters because investing is a behavioural activity. Markets don’t test our ability to download an app or compare returns. They test our patience during uncertainty, our discipline when prices fall and our willingness to stick to a long-term plan when short-term headlines suggest otherwise.

Technology can make investing faster.

It cannot make us calmer.

It can automate a SIP.

It cannot automate conviction.

The AirPod Effect, therefore, is neither a celebration nor a criticism of digital investing. It’s an attempt to understand what technology has genuinely improved and where it has quietly introduced new challenges.

Before discussing those challenges, however, it’s worth acknowledging something that often gets overlooked.

The AirPod generation has done many things remarkably well.

What the AirPod Generation Got Right

It’s easy to dismiss younger investors as impatient or overly dependent on technology.

That stereotype misses the bigger picture.

In reality, this generation has fundamentally improved the way investing is approached in India. They have challenged outdated assumptions, demanded greater transparency and embraced financial participation far earlier than previous generations.

They Democratized Investing

Perhaps the greatest achievement of the AirPod generation is that it made investing feel normal.

For previous generations, investing often required confidence that many first-time investors simply didn’t have. Visiting a bank branch, understanding financial jargon and filling out lengthy forms created friction at every stage of the journey.

Digital platforms changed that.

Today, a college graduate starting their first job can begin investing with a modest monthly SIP, complete KYC online and monitor their portfolio from a smartphone. Geography is no longer a barrier, and neither is prior financial experience.

Technology didn’t just simplify investing—it broadened participation.

In many ways, the biggest innovation wasn’t a new financial product. It was making existing products accessible to millions more people.

They Started Investing Earlier

Earlier generations often began investing only after major life milestones like marriage, buying a house or nearing retirement.

Today’s investors are starting much sooner.

That’s an important shift because TIME is one of the few advantages every investor can control.

Someone who begins investing in their twenties, even with relatively small amounts, benefits from years of compounding that simply cannot be recreated later in life. The amounts may be modest initially, but the habit itself is powerful.

Technology deserves some credit here.

When opening an investment account takes minutes instead of days, procrastination becomes harder to justify.

The biggest financial advantage of the AirPod generation may not be that they invest more.

It’s that they start earlier.

They Expect Transparency

Across every sector, the internet has completely transformed consumer expectations, and the financial services industry is experiencing the exact same shift.

Modern investors are continuously exposed to a vast wave of content, including social media posts, articles, and videos. Although this constant exposure does not necessarily grant them a profound understanding of intricate fund structures like expense ratios, it does ensure they absorb a great deal, prompting them to ask questions based on what they encounter.

Furthermore, technology intensifies this environment by allowing investors to view their fluctuating portfolio values directly on their mobile phones in real time. With every piece of advice being actively monitored and weighed against the live data on their screens, advisors cannot afford any complacency.

Ultimately, the true transformation lies not in investors becoming overnight experts, but in their expanded access to information, which enables them to ask more pertinent questions and expect absolute clarity, integrity, and thoughtfulness from their advisors.

They Take Ownership of Their Financial Decisions

One of the most significant cultural shifts has been the move from passive dependence to active participation.

Many young investors no longer assume that someone else will make financial decisions on their behalf. Instead, they seek information, evaluate alternatives and want to understand the reasoning behind every recommendation.

That doesn’t mean every decision is correct.

But it does represent a healthier mindset.

Financial literacy begins with curiosity, and curiosity begins with asking questions.

The AirPod generation has shown that investors don’t have to accept complexity as inevitable.

That’s a lesson the industry itself has benefited from.

Technology has undoubtedly made investing more accessible, transparent and inclusive. Those achievements shouldn’t be understated.

But accessibility and success are not the same thing.

Starting an investment has become remarkably easy.

Staying invested when markets become uncomfortable is an entirely different challenge.

And that is where the AirPod Effect reveals its other side.

When Convenience Becomes Overconfidence

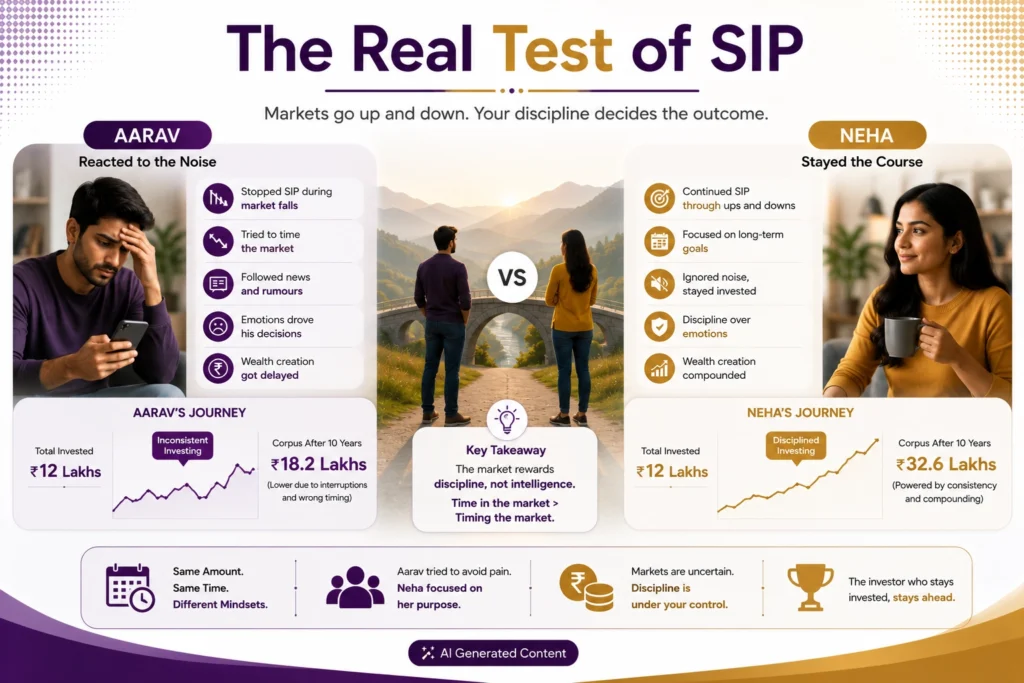

Aarav and Neha joined the same company within a month of each other. Both were 26, earned roughly the same salary, and shared similar financial goals. They wanted to build wealth over the long term, buy a home in the next decade, and eventually retire comfortably. After reading about mutual funds, each decided to start a ₹10,000 monthly SIP in a diversified equity mutual fund.

At first, their investment journeys looked almost identical.

Both completed their KYC online, chose the same fund, and set up automatic monthly investments through their phones. Neither had prior investing experience, and both believed they were making a sensible financial decision.

Three years later, however, their portfolios had begun to tell very different stories.

The difference was behavioural.

Technology has made investing equally easy for both of them. What separated their outcomes wasn’t the app they used, but how they responded when markets tested their emotions.

Convenience Is a Powerful Tool Until We Mistake It for Expertise

The popularity of SIPs is no accident.

They were designed to solve one of investing’s oldest problems: our tendency to make poor decisions when we try to predict short-term market movements.

Instead of asking investors to decide when to buy, a SIP automates the process. A fixed amount is invested at regular intervals, regardless of whether markets are rising or falling. This approach, known as rupee-cost averaging, helps investors accumulate more units when prices are lower and fewer when prices are higher, removing the pressure of trying to identify the “perfect” time to invest.

In other words, the system assumes something both humble and remarkably wise: most of us cannot consistently time the market.

Aarav understood another important reality.

His job was demanding. Between client meetings, deadlines, travel and family responsibilities, he didn’t have the time—or the desire—to track markets every day or analyse fund performance every month.

Rather than trying to become an investment expert overnight, he focused on understanding his financial goals and sought professional guidance to build a plan that suited his needs. Together, they decided on an appropriate asset allocation, selected investments aligned with his goals, and agreed to review the portfolio periodically instead of reacting to short-term market movements.

His SIP continued automatically, but he wasn’t investing on autopilot. He had simply delegated the decisions that required expertise while remaining involved in the decisions that mattered most—his goals, priorities and long-term plan.

Neha approached investing differently.

She enjoyed following financial news and investment influencers on social media. As markets moved, she became increasingly confident that she could spot patterns before everyone else.

When markets corrected sharply, she paused her SIP, convinced prices would fall further. A few months later, after markets recovered, she invested the accumulated amount as a lump sum because she believed the “worst was over.”

Sometimes she switched to whichever fund had delivered the highest returns over the previous year. Other times she exited investments because an expert online warned of an impending correction.

Each decision felt sensible at the time.

Together, however, they reflected several well-documented behavioural biases.

The Real Test of a SIP Begins When Markets Fall

A SIP is often described as a disciplined investment strategy, but discipline isn’t built into the product itself.

It’s built into the investor.

The easiest time to maintain a SIP is when markets are rising and portfolio values are increasing. The real challenge begins during periods of uncertainty, when every news alert seems to reinforce the fear that things might get worse before they get better.

Industry trends have consistently shown that SIP stoppages and mutual fund redemptions tend to increase during periods of sharp market volatility. AMFI’s monthly industry data has frequently reflected higher SIP discontinuations alongside elevated redemption activity during uncertain market conditions. While every correction is different, the behavioural pattern is remarkably consistent: confidence declines just when long-term investors are often presented with attractive buying opportunities.

This is where digital investing presents both an opportunity and a challenge.

On one hand, technology has made disciplined investing easier. Automatic bank mandates ensure that SIPs continue without requiring a monthly decision. Investors receive reminders, account statements and educational content that encourage regular participation.

On the other hand, the same technology provides constant visibility into short-term market movements.

Every notification.

Every price update.

Every viral social media post predicting either a crash or a rally.

Each one tempts investors to react.

Consider a simple illustration.

From our previous example, Aarav and Neha each planned to invest ₹10,000 every month over ten years.

Aarav stayed invested throughout.

Neha paused her SIP for twelve months during a prolonged market downturn, intending to invest the accumulated amount later when conditions felt “safer.”

Even if she eventually invested the same total amount, those missed months represented opportunities to buy more units at lower prices. Over time, the cost wasn’t simply 12 missed investments, it was the compounding benefit those investments could have generated over the years that followed.

The lesson isn’t that investors should ignore market risks.

It’s that repeatedly interrupting a long-term strategy often carries hidden costs that become visible only years later.

Investing Is as Much About Psychology as It Is About Markets

Behavioural finance reminds us that successful investing isn’t determined solely by choosing good investments. It also depends on creating systems that help us make better decisions.

One useful concept is mental accounting.

Aarav treated his SIP like any other monthly commitment. Once the money left his bank account, it became part of his long-term financial plan rather than money available for second-guessing. Regular reviews with his financial professional helped him focus on progress towards his goals instead of day-to-day market movements.

Neha, however, continued to see her SIP contribution as money she could redirect whenever markets became uncertain. Because it never felt fully committed, it remained vulnerable to short-term emotions.

Aarav effectively leveraged a “commitment device” to guide his investing. By automating his contributions and relying on a structured review schedule instead of tracking daily market fluctuations, he minimized the risk of making emotional choices. He did not hand over total responsibility; instead, he outsourced specialized expertise while continuing to make the final calls on his financial goals.

Neha, on the other hand, prioritized flexibility, viewing her SIP as money that could be easily redirected during times of market uncertainty. Because this capital never felt fully dedicated to a long-term plan, it remained highly vulnerable to short-term emotional impulses. Ultimately, that desired flexibility frequently transformed into a temptation to alter her strategy.

Ten Years Later

A decade after they began investing, Aarav and Neha met for coffee.

Both had grown in their careers. Both had navigated market rallies, sharp corrections, and major life milestones from promotions and home purchases to changing family responsibilities. Like every investor, they had experienced periods of uncertainty and moments of doubt.

Yet their financial journeys had unfolded differently.

Aarav’s portfolio reflected ten years of staying the course. The systems he’d built early on automating his investments, leaning on periodic reviews rather than daily market noise had simply run in the background while he focused on his career and life. He hadn’t needed to predict market movements; he’d needed to not interrupt the plan.

Neha was equally committed to building wealth, but her decade looked different. Each pause, each fund switch, each decision made in response to a headline or a friend’s opinion had felt reasonable in the moment. Collectively, though, they added up to a pattern: she was still searching for the right time to commit fully, ten years in.

What separated their outcomes wasn’t intelligence or access to information; both had the same tools and started from similar ground. It was that one of them had stopped needing to make decisions every time the market moved, and the other never quite did.

Investing Better: Practical Habits That Matter More Than Market Predictions

If the AirPod Effect has taught us anything, it’s this: technology has made investing remarkably easy, but it hasn’t made investing emotionally easy.

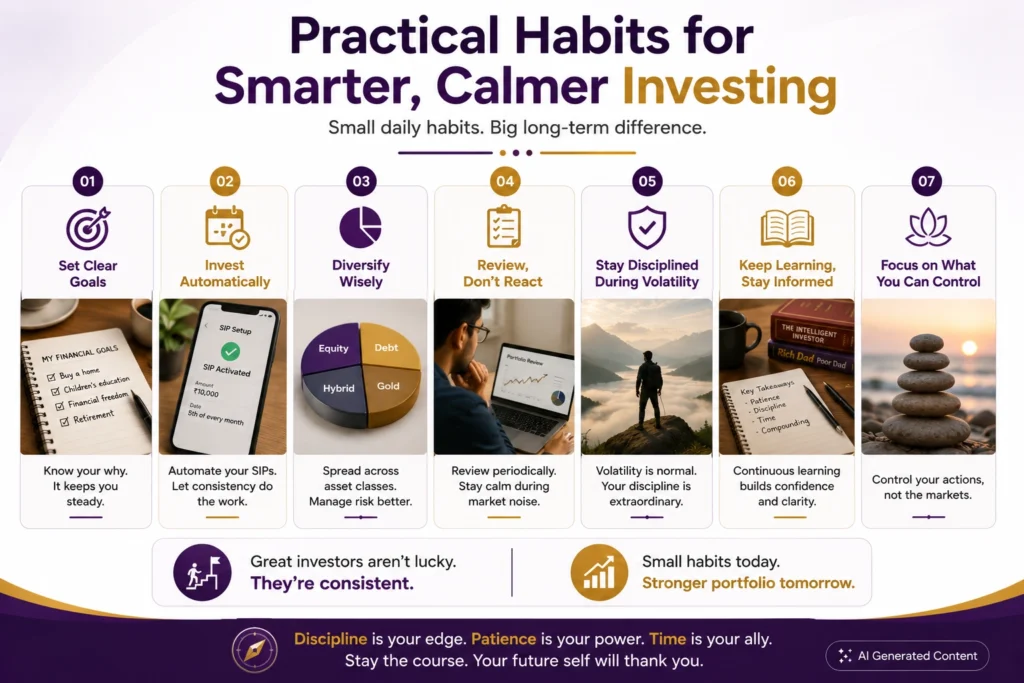

The good news is that successful investing doesn’t require predicting the next bull market or discovering the perfect mutual fund. More often than not, it comes down to building habits that help you make better decisions consistently.

Here are a few practical ways to do that.

1. Start With Your Goals, Not With a Fund

The first question shouldn’t be, “Which fund should I invest in?”

It should be, “What am I investing for?”

Your investment strategy should reflect your goals, whether that’s buying a home in seven years, funding your child’s education, building a retirement corpus, or creating long-term financial independence.

When you know why you’re investing, it’s much easier to stay committed during periods of market volatility.

A common obstacle: Investors often compare their portfolios with friends or social media influencers.

A better approach: Compare your investments only against your own financial goals. Someone else’s portfolio may have very different objectives, risk tolerance, and time horizon.

2. Let Automation Do the Heavy Lifting

A SIP is most effective when it becomes part of your monthly routine rather than a monthly decision.

Treat it like your rent, electricity bill, or insurance premium—a commitment that happens automatically.

Automation doesn’t remove market risk.

It removes decision fatigue.

For new investors, setting up an auto-debit mandate and reviewing investments only once or twice a year is often more effective than constantly monitoring market movements.

More experienced investors can gradually increase SIP contributions as their income grows, ensuring their investments keep pace with their financial aspirations.

3. Don’t Confuse Activity With Progress

One of the biggest myths in investing is that successful investors are constantly making changes.

In reality, many long-term investors succeed because they avoid unnecessary action.

Reviewing your portfolio is important.

Reacting to every headline isn’t.

Before making any investment decision, ask yourself three simple questions:

- Has my financial goal changed?

- Has my time horizon changed?

- Has my ability to take risk changed?

If the answer to all three is “no,” the best decision may be to stay the course.

4. Create Distance Between Emotion and Action

Technology has shortened the time between feeling an emotion and acting on it.

That’s why creating your own “pause button” is one of the most valuable investing habits you can develop.

If you’re tempted to stop a SIP or redeem investments because markets have fallen sharply, don’t act immediately.

Wait 24 hours.

Revisit your original investment objective.

Speak with someone you trust if needed.

Many impulsive decisions lose their urgency after a little time and perspective.

5. Keep Learning, But Choose Your Sources Wisely

The internet has made financial education more accessible than ever before.

It has also made misinformation easier to spread.

Educational resources from AMFI, SEBI’s investor awareness initiatives, and other credible financial institutions can help investors build a stronger foundation than relying solely on short-form social media content or market predictions.

The objective isn’t to know everything.

It’s to understand enough to make thoughtful decisions.

Know When to Seek a Second Opinion

One of the biggest misconceptions in investing is that asking for help means giving up control.

In reality, good financial guidance isn’t about someone else making decisions for you. It’s about having someone who can challenge your assumptions before emotions turn into expensive mistakes.

Technology is excellent at helping you execute transactions.

It cannot ask questions like:

- Does this investment still align with your long-term goals?

- Are you reacting to market headlines or responding to a genuine change in your circumstances?

- Have your financial priorities changed since you built this portfolio?

Sometimes, the most valuable advice isn’t a new investment recommendation.

It’s hearing someone say,

“Your plan still makes sense. Stay the course.”

Or,

“Let’s rethink this decision before making any changes.”

Professional guidance becomes particularly valuable during life’s major transitions—changing jobs, getting married, buying a home, planning for a child’s education, or approaching retirement. These moments often require decisions that go beyond choosing a mutual fund.

The goal isn’t to replace technology.

It’s to complement it with judgement, perspective and accountability.

Where SubhShanti Fits In

Throughout this article, one idea has appeared repeatedly: investing isn’t difficult because markets are unpredictable. It’s difficult because emotions are.

At SubhShanti Wealth, that’s where we believe guidance adds the greatest value.

We don’t see technology as competition—we use the same digital tools our clients use every day. They make investing faster, more transparent and more convenient.

Where we aim to make a difference is in the conversations that technology cannot have.

When markets become volatile.

When financial goals change.

When a major life decision requires balancing multiple priorities.

Or when an investor simply needs reassurance that staying invested is still the right choice.

Good financial guidance isn’t about predicting the next market move.

It’s about helping investors make thoughtful decisions consistently, even when emotions suggest otherwise.

That’s the spirit of SubhShanti—finding clarity amid uncertainty and staying focused on what truly matters.

Conclusion: The Best Investors Know When to Listen

The AirPod Effect has revolutionized investing by making it accessible and transparent. However, while technology has simplified how we invest, it hasn’t changed what success requires: the discipline to follow a plan despite market noise.

Superior outcomes arise when technology and professional guidance work together. Tech offers efficiency, while experts provide the perspective needed when markets become uncertain. This balance is central to SubhShanti Wealth.

Disclaimer

This article is produced for educational and investor-awareness purposes only. Nothing in this article constitutes investment advice, a recommendation to buy or sell any security or mutual fund, or a solicitation of any investment product.

All numerical illustrations, projections, and return scenarios presented in this article are hypothetical and for illustrative purposes only. They do not represent guaranteed or expected outcomes. Actual returns will vary depending on fund selection, market conditions, investment timing, and individual investor behaviour. Past performance of any fund, index, or market is not indicative of future results.

References to specific companies, IPO listings, or historical market events are factual and for educational context only. They do not constitute a recommendation or an opinion on those companies or securities.

The expense ratio difference between Direct and Regular Plans cited in this article is a general industry range and will vary by fund house and scheme. Investors should verify current expense ratios on the respective AMC website or AMFI’s official portal (www.amfiindia.com).

Before switching between Regular and Direct Plans, investors should consult a qualified tax professional or a SEBI-registered Investment Adviser to understand the capital gains implications. Short-term capital gains on equity fund redemptions are currently taxed at 20% (as at the date of this publication); this rate is subject to change.

AMFI-registered Mutual Fund Distributors and SEBI-registered Investment Advisers are separately regulated categories of professionals with distinct obligations under SEBI regulations. Investors are encouraged to verify the registration status of any financial professional through SEBI’s SCORES portal or AMFI’s official website before engaging their services.

The views expressed in this article are the author’s own and do not represent the views of AMFI, SEBI, or any fund house. This article has not been reviewed or approved by any regulatory authority.

Date of Publication: June 2026. Subject to periodic review and update.

SubhShanti Wealth Private Limited

AMFI Registered Mutual Fund Distributor | ARN – 331663