Over the past five years, healthcare costs in India have risen far faster than general inflation, with medical inflation staying around 13% to 14% annually. As treatment costs have climbed, health insurance premiums have also seen some of their sharpest increases in more than five years. That makes health insurance an essential part of financial planning today.

While life insurance safeguards your income, health insurance secures your savings. In a nation where out-of-pocket medical costs continue to soar, this distinction is not merely noteworthy but a strategic necessity.

Let’s explore why health insurance has become essential. It is a vital infrastructure.

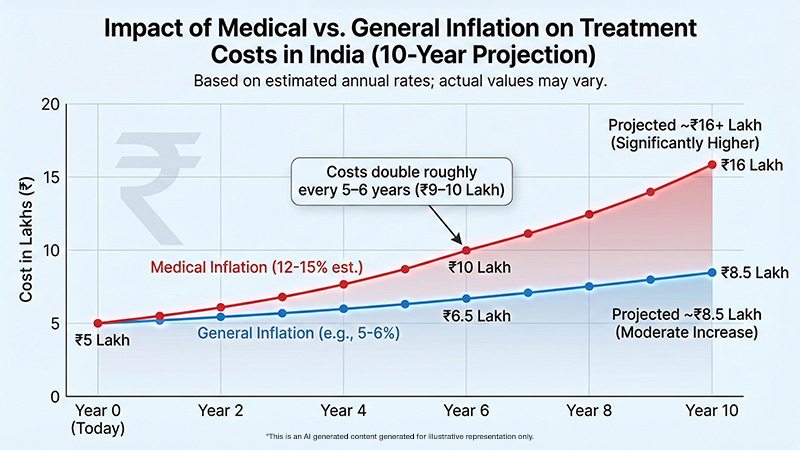

1. Medical Inflation

Medical inflation in India is estimated at 12–15% annually, significantly higher than general inflation. This means treatment costs double roughly every 5–6 years.

A surgery costing ₹5 lakh today may cost ₹9–10 lakh within a decade.

Data from the Insurance Regulatory and Development Authority of India and industry health reports consistently show rising hospitalization costs, especially in private healthcare.

One unexpected hospitalization can:

- Wipe out emergency savings

- Force premature withdrawal from investments

- Disrupt long-term financial goals

- Increase reliance on loans

Health insurance isn’t about pessimism; it’s about preventing medical expenses from derailing financial plans.

2. Cashless Treatment

Medical emergencies demand decisions, not fundraising.

Cashless hospitalization allows treatment at network hospitals without arranging large sums upfront. The insurer settles eligible expenses directly.

This means:

- No scrambling for funds

- No distress sale of assets

- No borrowing at high interest

- Faster access to quality care

In high-stress moments, liquidity is power. Cashless access provides it.

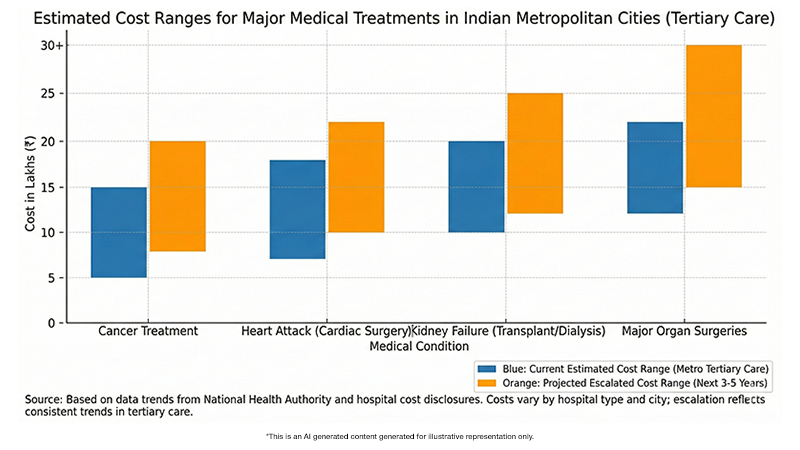

3. Coverage for Critical Illness & Major Surgeries

Serious illnesses aren’t rare events; they’re financial earthquakes.

Conditions such as cancer, heart attack, kidney failure, and major organ surgeries can cost anywhere between ₹5 lakh to ₹25 lakh or more, depending on the hospital and city.

According to data from the National Health Authority and multiple hospital cost disclosures, tertiary care treatments in metropolitan cities have seen consistent cost escalation.

Critical illness riders or standalone covers provide either reimbursement or lump sum payouts to help manage:

- Treatment expenses

- Recovery costs

- Income disruption during treatment

- Follow-up care

Healthcare advances are saving lives. Insurance ensures those advances do not bankrupt families.

4. Family Floater: Smart, Cost-Effective Protection

A family floater policy covers multiple family members under a single sum insured.

Instead of separate policies for each person, one consolidated cover protects:

- Spouse

- Children

- Dependent parents (if opted)

It is cost-effective and administratively simpler.

Statistically, not all members require hospitalization in the same year. A shared coverage pool often provides efficient protection at a lower premium compared to individual policies.

Efficiency is underrated in finance. A family floater embodies it.

5. Safeguards Your Investments

Without health insurance, a large hospitalization often forces:

- Breaking fixed deposits

- Redeeming mutual funds at the wrong time

- Liquidating long-term assets

- Taking high-interest loans

Health insurance prevents one medical event from undoing years of disciplined investing.

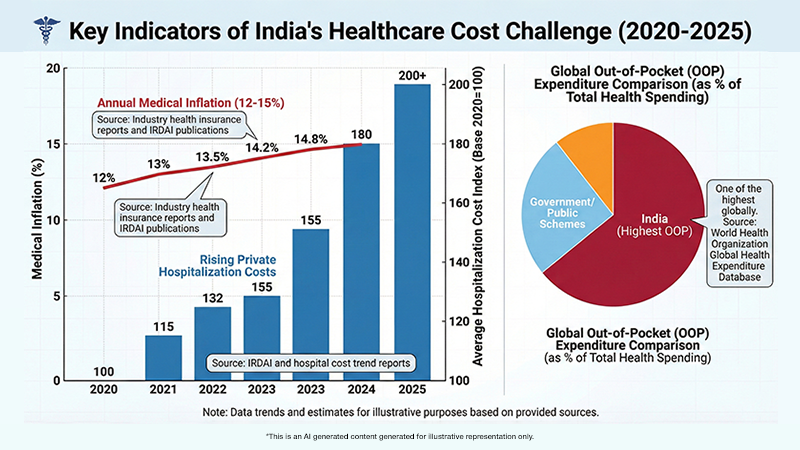

The Data Reality

• Medical inflation in India: ~12–15% annually

Source: Industry health insurance reports and IRDAI publications

• India continues to have one of the highest out-of-pocket healthcare expenditures globally as a percentage of total health spending

Source: World Health Organization Global Health Expenditure Database

• Rising hospitalization costs in private healthcare institutions

Source: IRDAI and hospital cost trend reports

The message is simple: healthcare costs are compounding faster than most investment portfolios.

Why You Should Consider Health Insurance

- You insure your future income through life insurance.

- You insure your wealth creation through investments.

- Health insurance protects the bridge between the two.

Without it:

One diagnosis can undo 10 years of disciplined investing.

With it:

- Savings remain intact.

- Goals remain funded.

- Dignity remains preserved.

Financial planning involves not only increasing your assets but also safeguarding them against foreseeable risks. Healthcare expenses can be expected, but their timing is uncertain, highlighting the importance of being prepared.

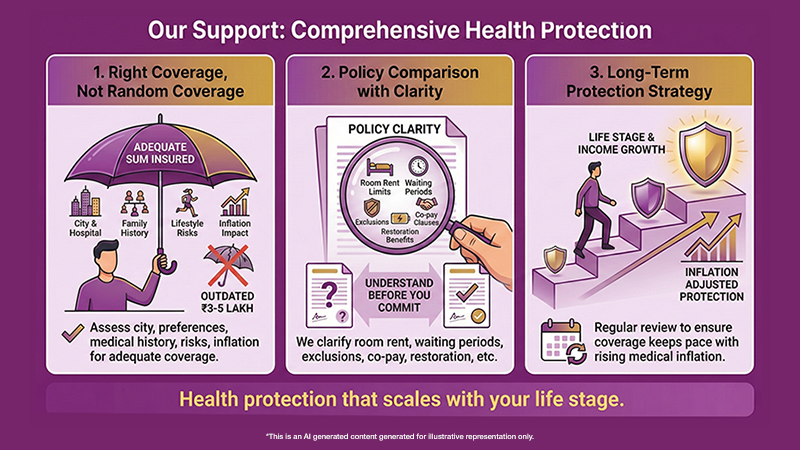

How SubhShanti Wealth Helps You Build a Strong Health Protection Plan

Health insurance is not about buying the cheapest premium. It is about choosing the right structure before a medical emergency chooses for you.

At SubhShanti Wealth, we treat health protection as a strategic layer in your overall financial plan.

Here’s how we support you:

1. Right Coverage, Not Random Coverage

We assess your city of residence, hospital preferences, family medical history, lifestyle risks, and inflation impact to recommend an adequate sum insured — not an outdated ₹3–5 lakh cover that may fall short.

2. Policy Comparison with Clarity

Room rent limits, waiting periods, exclusions, co-pay clauses, restoration benefits — most people discover these details at claim time. We help you understand them before you commit.

3. Long-Term Protection Strategy

As income grows and responsibilities evolve, we review your coverage to ensure it keeps pace with rising medical inflation. Health protection should scale with your life stage.

4. Easy Health Insurance Claim Support

SubhShanti Wealth helps make health insurance settlement simpler by supporting families through paperwork, insurer coordination, and claim-related follow-ups during medical emergencies. This reduces stress at a critical time and helps ensure that unexpected hospital expenses do not disturb long-term financial plans.

Medical emergencies are stressful enough. Financial confusion should not add to it.

If safeguarding your savings from rising healthcare costs is important to you, connect with SubhShanti Wealth. A structured conversation today can prevent a financial setback tomorrow.

Disclaimer

This article is intended solely for educational and informational purposes. It does not constitute investment advice, trading recommendations, or a solicitation to buy or sell any securities or financial instruments. The views expressed are based on publicly available data, regulatory studies, and industry observations, including reports published by the Securities and Exchange Board of India (SEBI). Readers are advised to assess their financial objectives, risk appetite, and suitability before making any investment or trading decisions. Derivatives trading, including Futures & Options (F&O), involves substantial risk and may not be suitable for all investors. Past performance is not indicative of future results. Investors should consult a SEBI-registered investment adviser or other qualified financial professional before acting on any information presented herein.