In boardrooms across the country, CXOs shape billion-dollar strategies, manage high-stakes decisions, and steward growth trajectories that define industries. But when it comes to personal wealth—even the most seasoned executives fall prey to misconceptions.

At SubhShanti Wealth, we’ve had the privilege of walking alongside more than a thousand clients, many of whom wear the CXO badge. Over time, we’ve observed an uncomfortable truth: professional success often masks personal blind spots, especially in wealth management.

This isn’t a cautionary narrative. It’s a strategic prompt—an opportunity to recalibrate, reassess priorities, and realign with long-term purpose.

Let’s unpack three critical miscalculations often made at the leadership level when it comes to wealth—and more importantly, explore the strategic pivots that turn misjudgment into mastery.

1. The Mistake of Confident Assumption

CXOs often possess superior analytical acumen. They can dissect P&Ls, anticipate market shifts, and evaluate strategic risk with precision. However, this same confidence—so valuable in the boardroom—can lead to complacency in their personal wealth management.

Many times, it is incorrectly assumed, the knowledge of corporate finance translates directly to personal finance expertise.

Unlike corporate finance, personal finance is all about aligning capital with life goals—fluid, emotional, often nonlinear.

Where This Goes Wrong:

- Over-diversification or under-diversification: Some CXOs spread their portfolios too thin across too many asset classes without understanding correlation.

- Overlooked planning: Legacy planning, succession structures and insurance often remain outdated or misaligned with wealth levels.

- Passive oversight: Delegating to a private banker without ongoing involvement often results in a templated, impersonal investment approach.

- Underestimating true risk appetite: A mismatch between actual risk capacity and assumed tolerance can quietly derail even the most disciplined plans.

The Shift:

Wealth literacy lies in understanding how capital behaves under pressure and how personal goals evolve with time. At SubhShanti Wealth, we advocate for portfolio mindfulness—a philosophy where every investment serves a purpose, and that purpose is revisited with intention as life and leadership evolve.

Reflective Question:

Are you actively steering your wealth strategy—or simply assuming it’s on the right track?

This is precisely where the role of a wealth expert shifts from execution to stewardship—a distinction we’ve detailed further in 5 Ways Wealth Experts Can Help Secure Your Financial Future.

2. The Trap of Active Earning

Consistent, high-velocity income can create a subtle blind spot: the assumption that inflows will always outpace needs. When wealth feels replenishable, long-term capital architecture often takes a back seat. But enduring affluence isn’t about how much you earn—it’s about how deliberately you convert earnings into lasting utility, freedom, and legacy.

The problem? Income is temporary. Wealth is permanent.

Your income may have built your lifestyle, but it’s your capital that must secure your legacy.

Where This Goes Wrong:

- Lifestyle creep: As earnings grow, so do expenses—(status growth) homes, cars, travel, and school fees. But few recalibrate their investments to match lifestyle inflation.

- Wealth-induced paralysis: The paradox of prosperity. When wealth arrives in waves, planning often stalls, as investors grapple with the scale and structure of newfound wealth.

- Overreliance on future liquidity: Wealth strategies often rely on unpredictable events like future promotions that lead to delaying wealth planning which means delayed compounding, limited allocation options, and unaddressed risks, leaving capital exposed and narrowing opportunities.

The Shift:

The moment your invested capital generates consistent passive income to cover your lifestyle, you’ve reached financial autonomy. This milestone should be your north star—not your CTC.

At SubhShanti Wealth, we help clients design what we call a Core Capital Framework—the amount you need invested across stable, tax-efficient instruments to sustain your life, irrespective of your job.

Reflective Question:

If your income stopped tomorrow, how long would your wealth sustain your current life?

3. The Misconception of Delegation as Clarity

Time poverty is real, especially for those running large enterprises. Between board meetings, travel schedules, investor calls, and family obligations, wealth often becomes a “weekend project”—one that never quite makes the calendar.

The mistake? Delegating wealth strategy to third parties without deliberate design.

High-performing professionals often outsource wealth to private banks or robo advisors. And while delegation is smart, abdication is not.

Where This Goes Wrong:

- One-size-fits-all portfolios: Robo advisors & private bankers operate on scale. Unless closely monitored, portfolios tend to mirror templated models, with little room for individual nuance.

- Misaligned Goals: A wealth strategy focused solely on transactions misses the opportunity for true transformation if it doesn’t incorporate explicit discussions about family, lifestyle, health, philanthropy, and legacy.

- Overlooking long-term transitions: Leadership transitions, sabbaticals, second innings, or relocation plans need wealth strategies that can flex—not just perform.

The Shift:

Engaging with your wealth does not mean checking markets daily or becoming a finance expert. It means investing in clarity—knowing what your capital is doing, why it’s doing it, and how it enables the life you want.

Reflective Question:

Is your current wealth setup truly personalized—or simply efficient?

Bonus Insight: The Emotional Cost of Wealth Neglect

CXOs often think of wealth in terms of numbers—assets, returns, goals, timelines. But beneath the spreadsheets lie emotions rarely addressed in quarterly reviews:

- Spouses who feel uninformed, or worse—excluded

- Children unclear on values or expectations

- Parents relying silently on your unstated support

- Guilt around not giving enough, or not living enough

At SubhShanti, we’ve learned that money is never just money.

It is an amplifier of values, of anxieties, of aspirations and when it’s left unspoken or unmanaged, it creates distance—not just in portfolios, but in families.

That’s why wealth planning must evolve beyond technical strategy.

It must become emotionally intelligent.

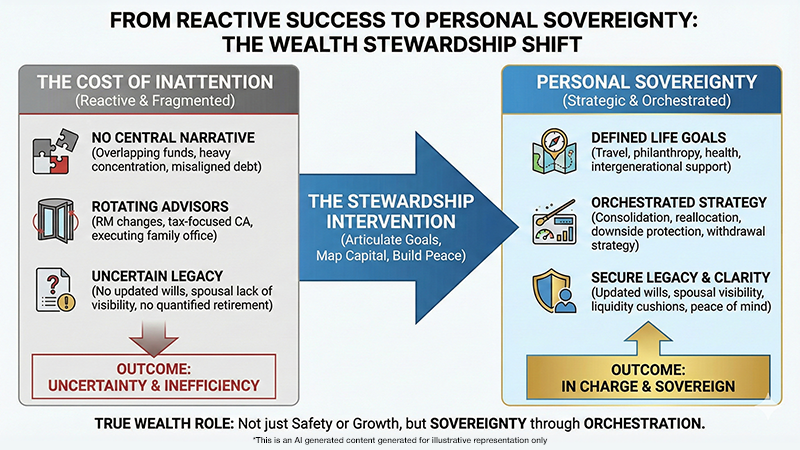

Real Case Study

- From Professional Success to Personal Sovereignty

(Anonymized for confidentiality)

R. Mehra, a 47-year-old COO in the FMCG sector, came to us with ₹18 crore in assets—but no real plan. He’d invested diligently, but reactively. His wife had no visibility into their holdings. Their wills hadn’t been updated in a decade. (There was no will, no legacy planning done) Their retirement lifestyle hadn’t been quantified.

We initiated three sessions with both spouses:

- Session 1: Articulating life goals—travel, philanthropy, health, intergenerational support

- Session 2: Mapping capital to intent—consolidation, reallocation, withdrawal strategy

- Session 3: Building peace—legacy plan, spousal clarity, and liquidity cushions

Within six months, Mr. Mehra didn’t just feel “secure.”

He felt in charge—of his future, his relationships, and his time.

That’s the true role of wealth.

Not just safety. Not just growth. But sovereignty.

- The Cost of Inattention: Case of the High-Performance, Low-Yield Portfolio

One of our early clients was the CTO of a global tech firm. By all markers, he had “done it right”—early ESOPs, multiple investments, international exposure, a family office structure, and a large inflow from a recent stake sale.

Yet when we ran his portfolio through our diagnostic lens, the findings were sobering:

- Multiple overlapping fund positions with no unified asset allocation

- Heavy equity concentration with no downside protection strategy

- Long-term debt holdings that were misaligned with his cash flow needs

- A total absence of estate or legacy planning despite a growing family

When we asked why, his response was typical:

“I thought my RM was handling it.”

But the RM was rotating every 14 months.

The CA was focused on tax filings, not wealth planning.

And the family office was simply executing instructions, not interpreting life events.

In short, everyone was managing parts. No one was stewarding the whole.

Wealth, like an enterprise, needs a central narrative. And that narrative can only come from you.

As portfolios scale in size and complexity, the challenge shifts from access to orchestration—a nuance especially relevant when considering alternatives, as discussed in our article Top Alternative Investments in High-Net-Worth Portfolios.

From Earning Capacity to Capital Capacity

Wealth, unlike career progression, does not follow a promotion path. It bends, curves, and often contradicts the patterns we are trained to seek. A CXO’s challenge is not earning more—it is converting surplus into sovereignty.

Here’s a reframe to consider:

| Traditional Insights | Evolved Insights |

| I’m already informed | I’m always evolving |

| My income is my strength | My capital is my fortress |

| I don’t have time | My wealth deserves time |

What Should be your Next Step?

If any of the above sounded uncomfortably familiar, here’s what we recommend:

1. Audit Your Life Goals Quarterly

Your wealth management should adapt as your life changes, not just your investment portfolio.So must your wealth plan. Block time every quarter to ask: “Is my wealth serving my life’s current chapter?”

2. Insist on a Human-Centric Strategy

Beyond algorithms and dashboards, ensure your strategy considers relationships, values, and transitions. Technology is an enabler—not a substitute for intent.

3. Design for Legacy Early

Begin now. A well-designed estate plan or philanthropic vehicle can enhance—not limit—your financial freedom.

Disclaimer

This article is intended solely for educational and informational purposes. It does not constitute investment advice, trading recommendations, or a solicitation to buy or sell any securities or financial instruments. The views expressed are based on publicly available data, regulatory studies, and industry observations, including reports published by the Securities and Exchange Board of India (SEBI). Readers are advised to assess their financial objectives, risk appetite, and suitability before making any investment or trading decisions. Derivatives trading, including Futures & Options (F&O), involves substantial risk and may not be suitable for all investors. Past performance is not indicative of future results. Investors should consult a SEBI-registered investment adviser or other qualified financial professional before acting on any information presented herein.