Let’s be honest, the high-income earners, self-made professionals, and wealth-focused families out there. You’re not investing just to make returns. You’re investing in the hopes to become rich and for the most sought out thing in the world, ‘financial security’.

And in that game, mutual funds are the stealth players—quietly compounding, legally sheltering, and tactically moving your money without setting off tax alarms or liquidity landmines.

Most investors never explore beyond SIPs and “how much return did I make this year?”

But today, we’re going deeper. Let’s unlock five underrated, under-leveraged, and absolutely legal advantages of mutual funds in India.

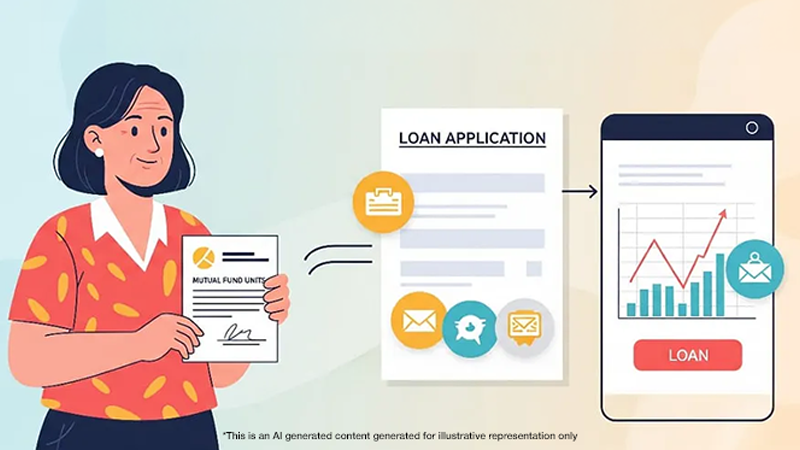

1. Get Loans Against Your Mutual Fund Units—Without Selling

Need money fast, but hate the idea of selling your investments?

Enter the unsung hero: loans against mutual funds.

You can now pledge your mutual fund units—whether equity or debt—as collateral and get a loan approved in record time. No heartbreak of redeeming. No capital gains tax. No disruption in compounding.

It’s like getting a cash advance without breaking the engine that creates it.

How It Works:

- Approach a bank or NBFC and pledge your units

- They assess your NAV (Net Asset Value)

- Get a loan up to 50–70% of your holdings

- Your funds stay invested and growing—while you get liquidity

Who Should Consider This:

- Professionals needing short-term cash for business or emergencies

- HNIs managing complex cash flows

- Anyone who understands that redemption is not the only option

2. Tax Loss Harvesting: Turn Market Dips into Tax Wins

Let’s talk about turning loss into tax-saving loss.

Tax Loss Harvesting is the art (and science) of selling underperforming investments to book a loss, which can then be used to offset capital gains elsewhere. It’s a strategy every portfolio manager knows—but most retail investors ignore.

Let’s say:

- You booked ₹2 lakh in gains from a fund

- But you’re also holding a dud that’s down ₹50,000

- Sell the dud, book the loss

- Now your taxable gain is just ₹1.5 lakh

Boom. That’s smart tax planning, not just smart investing.

3. Mutual Funds Are Exempt from Wealth Tax in India

No one likes the word “tax.” But we especially don’t like wealth tax—the idea of being taxed not just on what you earn, but on what you already own.

Here’s the kicker:

Mutual fund holdings are exempt from wealth tax.

Yes, wealth tax was abolished in 2015. But seasoned investors plan with one eye on the past and another on the future. Because tax laws evolve—and what’s gone can come back in a shinier, sneakier form, you never know.

Thanks to Section 10(23D) of the Income Tax Act, mutual funds remain one of the cleanest, least-taxed asset classes in your arsenal.

Why This Matters:

- No erosion of wealth due to yearly taxes on fund holdings

- Compounding happens undisturbed—no “tax drag” at the fund level

- Elites, NRIs, and family offices can structure assets more efficiently

4. Mutual Funds for Children: The New-Age Gift That Grows Up With Them

Forget gold coins and fixed deposits. You want to give your child a head-start?

Start a mutual fund.

Yes, you can invest in your child’s name, and funds for education, marriage, or their first big dream—even if that dream is studying space law in Japan.

What Makes It Magical:

- Equity mutual funds beat inflation over long horizons

- Debt and hybrid options offer safety and stability

- You can make it part of a SIP—automated, disciplined, goal-linked

- Over time, it teaches kids the value of investing

In a world where children learn faster than ever, a mutual fund is both a financial gift and a life lesson.

5. Mutual Funds as Inheritance Tools: Smooth Succession, Zero Drama

If you’ve ever watched a family squabble over land or gold—you know inheritance can get messy.

With mutual funds? It’s clean, digital, and drama-free.

Why It’s a Dream for Estate Planning:

- Nominee can be easily added or changed

- Transmission of funds doesn’t require probate (if nominee exists)

- Easy for legal heirs to trace, claim, and manage

- No physical handling, no locker stress, no value disputes

Want to pass on wealth, not headaches?

This is your answer.

This simplicity becomes even more powerful when viewed in the broader context of succession planning—where many families make avoidable mistakes, as outlined in Common Mistakes UHNWIs Should Avoid When Planning to Transfer or Preserve Wealth.

The Strategic Use of Mutual Funds

Mutual funds in India are no longer just a “middle-class investment product.”

They’re now part of a smart wealth strategy for people who understand agility, tax intelligence, and liquidity control.

When you combine:

- Collateral-backed loans

- Tax-loss harvesting

- Wealth tax exemption

- Child-centric planning

- Inheritance readiness

You don’t just have a product. You have a financial ecosystem that builds, guards, and multiplies your money.

At higher portfolio levels, mutual funds often form the core layer—while more specialised instruments like PMS, AIFs, and SIFs are used to add precision and complexity, a structure we explore further in Top Alternative Investments in High-Value Portfolios.

FAQs

Q: Are all types of mutual funds eligible for loans and tax benefits?

Yes. Most equity, debt, hybrid, and even liquid funds can be pledged for loans. Tax benefits apply differently depending on your holding period and asset type.

Q: Does tax loss harvesting apply to SIPs too?

Absolutely. SIPs are just staggered purchases. You can redeem specific loss-making units without affecting the rest. Just be mindful of the holding period to avoid short-term tax impact.

Q: Is wealth tax permanently gone in India?

For now, yes—it was abolished in 2015. But the principle of choosing tax-resilient instruments still applies. Mutual funds are protected under Section 10(23D) and are one of the most defensible assets even if tax policies change.

Q: Can I invest in mutual funds specifically for my child?

Yes. You can start SIPs or lump-sum investments in your child’s name or goals within your own portfolio. Some AMCs also offer “child-focused” funds with lock-ins and goal tracking.

Final Word: Mutual Funds Aren’t Just for Returns—They offer much more.

It’s not about finding the next “hot” or “trending” mutual fund.

That’s a distraction. A surface game.

Mutual funds, when used strategically, become more than products.

They become a system—for growth, protection, access, and legacy.

These aren’t just tools for saving money.

They’re engines of silent wealth creation, shielding you from tax friction most investors don’t even realize exists.

They give you liquidity when life calls—without disrupting your long-term plans. They help you raise capital without selling your soul—or your holdings.

And they let you pass on wealth without courtrooms, confusion, or chaos.

If you’ve been treating mutual funds like “just another investment,” you’re missing the plot.

Because when used right, they’re the entire financial playbook:

- They help you grow, without bleeding.

- They help you access, without breaking.

- They help you optimize, without overthinking.

They are not trendy. But timeless.This isn’t about market timing.

This is about life-timing.

And mutual funds are the one instrument that show up for both.

Disclaimer

This article is intended solely for educational and informational purposes. It does not constitute investment advice, trading recommendations, or a solicitation to buy or sell any securities or financial instruments. The views expressed are based on publicly available data, regulatory studies, and industry observations, including reports published by the Securities and Exchange Board of India (SEBI). Readers are advised to assess their financial objectives, risk appetite, and suitability before making any investment or trading decisions. Derivatives trading, including Futures & Options (F&O), involves substantial risk and may not be suitable for all investors. Past performance is not indicative of future results. Investors should consult a SEBI-registered investment adviser or other qualified financial professional before acting on any information presented herein.