A Crorepati Calculator helps you determine the monthly SIP amount needed to accumulate ₹1 crore (or more) by a target age, factoring in returns, inflation, and existing savings. These tools are popular in India for long-term wealth planning via mutual funds.

How It Works

Enter:

- Target amount (e.g., ₹1 crore today)

- Current age and target crorepati age

- Expected SIP return rate (typically 10-15%)

- Inflation rate (usually 5-7%)

- Existing savings

The calculator adjusts the target for inflation, grows your current savings, then computes the required monthly SIP using the SIP formula.

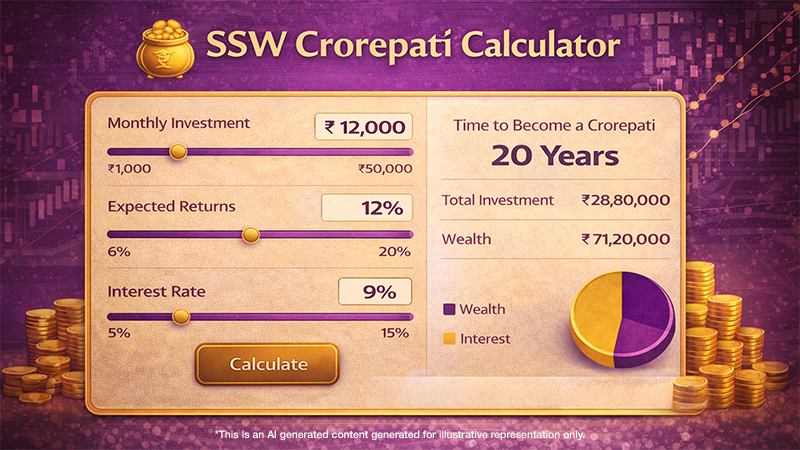

SSW Crorepati Calculator

Example: For someone aged 30 wanting ₹1 crore (today’s value) by age 50:

- Expected return: 12% p.a.

- Inflation: 6% p.a.

- Existing savings: ₹100000

Results:

| Parameter | Value |

| Years needed | 20 |

| Inflation-adjusted target | ₹3.20 crore |

| Monthly SIP required | ₹33,817 |

| Total invested | ₹81.16 lakh |

| Total growth | ₹2.29 crore |

This shows ₹33,817/month at 12% can make you a crorepati in 20 years.

Benefits

- Reveals realistic SIP amounts for big goals.

- Accounts for inflation to maintain purchasing power.

- Encourages disciplined investing via SIPs.

Use SSW’s crorepati calculator to personalise your plan — start small, stay consistent, and compound your way to ₹1 crore.

SSW Become a Crorepati Calculator FAQs

1. Can I become a crorepati if I start late (age 45+)?

Yes. Starting late means investing more, not giving up.

₹50,000/month at 12% for 15 years can grow to ~₹1.9 crore.

If you have only 10 years, the SIP needs to be higher—around ₹1.5 lakh/month.

2. What if markets crash midway—will ₹1 crore still happen?

Market falls don’t break SIPs; panic does.

SIPs benefit from rupee-cost averaging, buying more units during crashes.

Even the 2008 crash recovered in about 3 years. Staying invested matters more than timing.

3. What does ₹1 crore today mean after 20 years (inflation-adjusted)?

To maintain your current lifestyle, a ₹1 crore corpus must grow to ₹3.2 crore in 20 years just to offset a 6% annual inflation rate. That’s why targets must be inflation-adjusted—otherwise, goals look achieved but feel short.

4. Debt funds or equity for becoming a crorepati?

Equity is essential for long-term wealth creation.

At 12–15% (equity), you may need ~₹35,000/month.

At 7–8% (debt), you may need ~₹80,000/month for the same goal.

Debt alone is usually too slow for big goals

5. How powerful is a Step-Up SIP with salary hikes?

Very. Start with ₹20,000/month and increase it by 10% every year.

In 15 years, this can grow to ~₹1.6 crore, with total investment of only ~₹76 lakh. This mirrors real career growth and keeps SIPs realistic.

Disclaimer

The above results are for illustration purposes only. Please get in touch with a professional advisor for a detailed suggestion. The calculations are not based on any judgments of the future return of the debt and equity markets / sectors or of any individual security and should not be construed as a promise on minimum returns and/or safeguard of capital. While utmost care has been exercised while preparing the calculator, SSW does not warrant the completeness or guarantee that the achieved computations are flawless and/or accurate and disclaims all liabilities, losses and damages arising out of the use or in respect of anything done in reliance of the calculator. The examples do not purport to represent the performance of any security or investments. Given the individual nature of tax consequences, each investor is advised to consult his/her professional tax/financial advisor before making any investment decision. Past performance may or may not be sustained in future and is not a guarantee of any future returns.

The information/illustrations provided herein is meant only for general reading purposes and the views being expressed only constitute opinions and therefore cannot be considered as guidelines, recommendations or as a professional guide for the readers. The document has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. The sponsor, the Investment Manager, the Trustee or any of their directors, employees, associates or representatives (‘entities & their associates”) do not assume any responsibility for, or warrant the accuracy, completeness, adequacy and reliability of such information. Recipients of this information are advised to rely on their own analysis, interpretations & investigations. Readers are also advised to seek independent professional advice in order to arrive at an informed investment decision. Entities & their associates including persons involved in the preparation or issuance of this material, shall not be liable in any way for any direct, indirect, special, incidental, consequential, punitive or exemplary damages, including on account of lost profits arising from the information contained in this material. Recipient alone shall be fully responsible for any decision taken on the basis of this document

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.