The most effective technique for worry-free golden years

Retirement planning is no longer a luxury or a “future problem.” It is a present-day responsibility. Indians are living longer, healthcare costs are rising faster than inflation, and traditional family support structures are quietly thinning. Many people will now spend 20 years or more without a regular salary.

Yet, most retirement conversations still begin too late.

For a large section of Indians, retirement savings are limited to statutory schemes like EPF or NPS. These are valuable foundations, but on their own, they often fall short of sustaining lifestyle, dignity, and independence over decades. This gap is where Systematic Investment Plans (SIPs) quietly do their most important work.

SIPs offer a disciplined system that turns time, consistency, and markets into a long-term retirement engine.

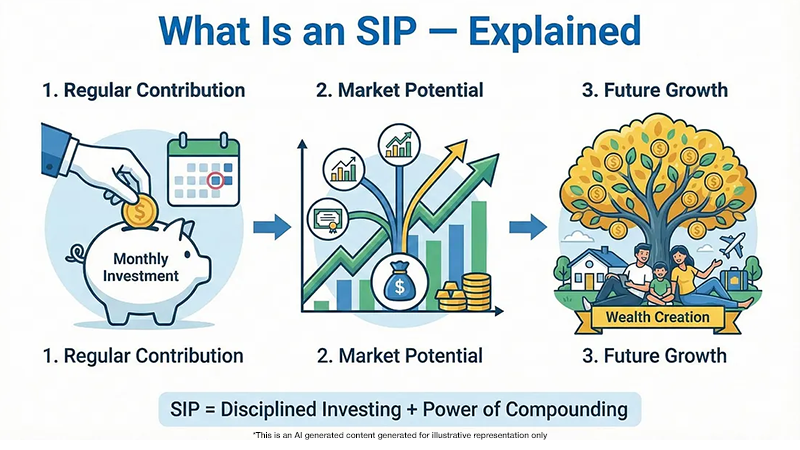

What Is an SIP — Explained

A Systematic Investment Plan (SIP) is a method of investing a fixed amount regularly—monthly, weekly, or even daily into a mutual fund. Instead of trying to guess market highs and lows, you invest consistently at prevailing prices.

This long-term, disciplined strategy replaces emotional reactions in investing with a consistent habit. Instead of trying to “time the market” or being deterred by negative news cycles, you simply maintain your investment schedule.

That simplicity is precisely why SIPs work so well for long-term goals like retirement.

Why SIPs Work for Retirement (The Engine Room)

SIPs succeed not because markets always rise, but because of how they behave across time.

- Rupee-Cost Averaging

When markets are volatile, SIPs automatically buy more units at lower prices and fewer units at higher prices. This evens out your cost over time and reduces timing risk. - Compounding

Returns don’t just add up—they multiply. Earnings generate their own earnings, and over long periods, this effect becomes exponential. Compounding rewards patience far more than brilliance. - Discipline Over Emotion

SIPs automate good behaviour. They prevent panic during market falls and overconfidence during rallies—two of the biggest destroyers of retirement wealth.

For retirement planning, this behavioural advantage is as important as returns.

A Short History: How SIPs Became Mainstream in India

India’s mutual fund journey helps explain why SIPs are now central to retirement planning.

• 1963 – Unit Trust of India (UTI) launched India’s first mutual fund

• 1987 – SBI Mutual Fund entered, expanding access beyond UTI

• 1992–93 – SEBI regulation brought transparency and private participation

• Mid-1990s – Early versions of SIPs were introduced

• 2010s onward – Awareness campaigns like Mutual Funds Sahi Hai normalised SIPs for everyday savers

What began as a niche product gradually became a mass habit, transforming mutual funds from speculative tools into long-term savings vehicles.

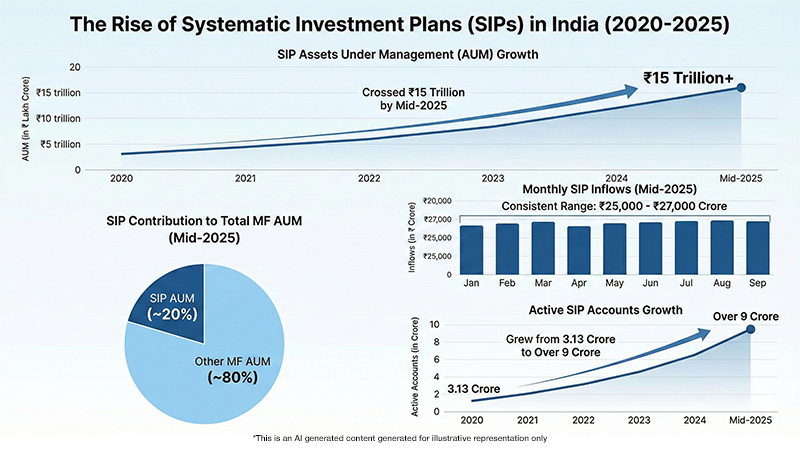

The Current SIP Landscape: Why This Matters

The numbers today tell a powerful story of structural change.

• SIP Assets Under Management crossed ₹15 trillion by mid-2025

• SIPs now contribute nearly 20% of the mutual fund industry’s total AUM

• Monthly SIP inflows consistently range between ₹25,000–₹27,000 crore

• Active SIP accounts grew from 3.13 crore in 2020 to over 9 crore by 2025

This reflects a generational shift toward disciplined, long-term investing, especially for retirement.

India’s Retirement Reality

India faces a unique retirement challenge.

Only a small portion of the workforce is covered by formal pension systems. A vast informal sector has little or no structured retirement support. At the same time, life expectancy is rising steadily.

Many Indians will spend 15–25 years in retirement, often with increasing medical and lifestyle expenses but limited predictable income.

In this environment, retirement security cannot depend on one instrument alone. Funding retirement through a SIP is effective because it combines essential elements: personal ownership, a long-term perspective, and the use of growth-oriented tools.

A simple illustration.

An individual starts investing ₹10,000 per month at age 30 and continues till age 60—30 years of consistency.

• Total contribution over 30 years: ₹36 lakhs

• At a long-term average return of ~12%, the potential value can grow to well over ₹3.1 crore

• With higher long-term equity participation, outcomes can be meaningfully higher

The core lesson here is the asymmetry: allowing time and compounding to work uninterrupted means that even relatively small, consistent monthly contributions can result in a significantly large retirement corpus.

This is why starting early matters more than starting big. For retirement investors, the real risk is not market volatility. It is stopping, delaying, or constantly second-guessing.

SIPs Across Income Groups: One Tool, Many Lives

– Low-Income & Emerging Middle Class

SIPs can begin with very small amounts. Micro-SIPs starting at ₹100–₹500 per month allow first-time investors to build habits, not just portfolios.

– Middle & Higher-Income Groups

Step-up SIPs allow contributions to grow alongside income, ensuring retirement savings keep pace with lifestyle aspirations.

– Women & First-Time Investors

Regulatory initiatives and digital platforms have expanded access, making SIPs a powerful inclusion tool—especially for those with career breaks or irregular income.

The strength of SIPs lies in their adaptability.

While retirement is a long-term priority, many investors must simultaneously plan for equally important milestones such as a child’s education. SIPs work especially well here because they allow parallel goal-based investing without sacrificing one objective for another. We explore this balance in detail in our blog, 5 Steps to Structure SIPs for Your Child’s Education & Stay on Track which explains how families can structure education-focused investments alongside retirement planning with clarity and discipline.

SIPs and Other Retirement Tools: Playing Different Roles

Retirement planning works best when tools are combined thoughtfully.

- SIPs provide long-term growth and inflation protection

- EPF / NPS provide stability and discipline

- Gold and real assets act as hedges

- FDs and traditional savings offer certainty but limited growth

Each tool solves a different problem. SIPs address the most critical one: growth over time. As retirement approaches, asset allocation can gradually shift toward debt and hybrid funds to protect accumulated gains.

The Data Shows

Longer holding periods among SIP investors indicate improving financial maturity. While stoppages occur, much of this reflects account clean-ups rather than panic exits.A rise in financial maturity is suggested by the longer duration SIP investors are holding their investments. Also, SIP stoppages often occur due to account maintenance rather than panic selling.

The trend is clear: investors who treat SIPs as long-term commitments are staying invested longer, a crucial ingredient for retirement success.

From Accumulation to Income

Building a retirement corpus is only half the journey. The second half is using it wisely.

This is where a Systematic Withdrawal Plan (SWP) becomes important.

An SWP allows retirees to withdraw a fixed amount regularly from their mutual fund investments, creating a predictable income stream while the remaining corpus stays invested and continues to grow.

When structured thoughtfully, SWPs can:

• Provide steady post-retirement cash flow

• Reduce the risk of withdrawing too much too soon

• Help manage taxes more efficiently

• Extend the life of the retirement corpus

Saving for retirement via SIPs is just the start. The true challenge is the shift from accumulation to distribution when regular income ends. This phase requires a structured withdrawal strategy to manage cash flow, portfolio longevity, and tax efficiency. This is where Systematic Withdrawal Plans come in, explained in detail in our blog, How SWP Turns Your Retirement Corpus into a Paycheque, which walks through how retirees can convert accumulated wealth into a predictable, sustainable income stream without dismantling the portfolio.

SIPs Are Not Exciting — They Are Effective

SIPs are a system built for investment that prioritises consistent growth over market timing. They help turn regular income into a foundation for future financial freedom, offering millions in India a long-term path to wealth creation.

Retirement is not just about reaching a number, it is about sustaining freedom, dignity, and choice for decades after your last salary.

In that journey, SIPs remain one of the most reliable engines India has ever built for everyone.

Disclaimer

This article is intended solely for educational and informational purposes. It does not constitute investment advice, trading recommendations, or a solicitation to buy or sell any securities or financial instruments. The views expressed are based on publicly available data, regulatory studies, and industry observations, including reports published by the Securities and Exchange Board of India (SEBI). Readers are advised to assess their financial objectives, risk appetite, and suitability before making any investment or trading decisions. Derivatives trading, including Futures & Options (F&O), involves substantial risk and may not be suitable for all investors. Past performance is not indicative of future results. Investors should consult a SEBI-registered investment adviser or other qualified financial professional before acting on any information presented herein.