Starting your journey in wealth management in India can feel like stepping into a gym for the first time. The weights look heavy, the machines confusing, and everyone around you seems to know exactly what they’re doing.

What if we say : You don’t have to lift it all at once. In fact, you can live your life as you desire and have the peace of mind to focus on what truly matters. All it takes is the right guidance, a sound plan, and the consistency to stick with it.

Wealth management in India is no longer a luxury reserved for ultra-rich families—it’s a necessity for anyone who wants to create clarity in their finances and build a future without money anxiety. Whether you’re a salaried professional, a first-time entrepreneur, or someone who has already built wealth and now wants to protect it, this journey starts with a single step: understanding.

The wealth management industry in India is experiencing unprecedented growth, with Deloitte projecting a remarkable US$1.6 trillion AUM growth opportunity for wealth management service providers between FY24 and FY29. This surge is attributed to rising affluence, expanding middle class, and changing investment behaviors across customer segments .

Here’s your step-by-step guide to start financial planning in India—the humane, practical way.

Step 1: Define Your “Why” Before Your “What”

Most beginners jump straight to the “what”: Which mutual fund should I buy? Should I invest in gold? Real estate?

But the real starting point of goal-based financial planning in India is asking why.

Why do you want to invest?

- Is it for financial security, early retirement, or a child’s education?

- What does money mean to you—freedom, safety, or legacy?

Your “why” becomes the compass. The “what” (products) and “how” (strategies) follow naturally. Financial planning provides direction to your goals in life, and achieving something in life often demands strategic investment.

Step 2: Build the Foundation (Emergency Fund & Insurance)

No skyscraper stands without a strong base. Likewise, no wealth plan survives without safety nets.

Emergency Fund: Keep at least 6 months’ expenses in a liquid option (bank savings or liquid mutual funds). This financial cushion protects you from unexpected events and maintains your family’s financial stability.

Insurance: Health and term life cover aren’t expenses—they’re financial shields. Life insurance provides protection for your family while investment-linked insurance plans like ULIPs offer both risk cover and investment opportunities.

Step 3: Explore Your Investment Options (Aligned to Life Stage & Risk Appetite)

Wealth management in India offers a buffet—mutual funds, NPS, fixed deposits, bonds, PMS, AIFs, even startup investing. But the trick is not in chasing “the best” product; it’s about finding the best fit for you.

Investment Options for Different Life Stages:

Young Professionals → SIPs, index funds, and goal-based planning

- Mutual funds are ideal for beginners who find stock investing confusing

- SIP (Systematic Investment Plan) allows you to invest small amounts regularly

Mid-Career Professionals → Balanced allocation with tax-efficient investments

- Mix of equity and debt funds based on risk tolerance

- Fixed deposits for stable, guaranteed returns

Entrepreneurs → Liquidity on demand + separation of business vs personal wealth

- Focus on maintaining cash flow while building long-term wealth

CXOs / HNIs → Legacy planning, global diversification, and alternate investments

- The number of high-net-worth individuals in India is expected to rise by 75%, from 3.5 lakh in 2020 to 6.11 lakh by 2025

Step 4: Harness the Power of Compounding

Albert Einstein allegedly called compounding the “eighth wonder of the world.“

Example according to SEBI:

- ₹10,000 per month for 20 years at 12% CAGR = ~₹1 crore

- ₹10,000 per month for 30 years at the same rate = ~₹3.5 crores

The extra 10 years don’t just add—they multiply. The earlier you start investing in India, the stronger your future wealth becomes. This is the magic of compound interest working in your favor.

Step 5: Don’t Go At It Alone

DIY apps are great for first steps, but wealth management is not just about picking funds. It’s about strategy, reviews, and behavioral discipline.

A wealth manager in India acts as your coach, guiding you through market emotions. Research by DALBAR shows investors underperform markets because they buy high and sell low. A trusted partner helps you stay the course and make informed financial decisions.

Benefits of Professional Financial Planning:

- Enhanced returns on investment through strategic planning

- Better cash flow management and reduced overhead costs

- Risk assessment and liability management

- Retirement readiness and long-term security

Step 6: Keep Reviewing, Keep Adapting

Life evolves—careers, marriages, children, relocations. So should your portfolio. A yearly review isn’t about chasing performance; it’s about realigning to goals.

Financial planning is a dynamic journey that demands consistent review and refinement. As your income expands and your life evolves—whether through career milestones, family changes, or new responsibilities—your investment strategy must adapt to reflect these shifting priorities. This is especially true when wealth management extends beyond personal goals to encompass your entire family’s financial security.

Building wealth for your family requires thoughtful coordination between your immediate needs and long-term aspirations. For a comprehensive roadmap on initiating this process, explore our guide on Things to Do If You Want to Start Wealth Planning for Your Family, which breaks down the essential steps to establish family-focused financial strategies.

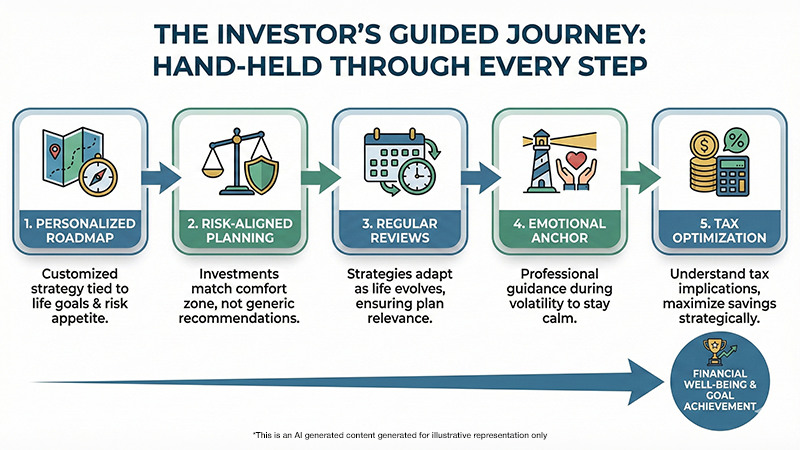

How SubhShanti Wealth Adds Value in Your Wealth Management Journey

The difference between simply “investing” and truly “managing wealth” lies in care, consistency, and customization. That’s where SubhShanti Wealth stands apart.

Here’s how we hand-hold every investor through their unique journey:

- Personalized Roadmap: Every client receives a customized strategy tied to their life goals and risk appetite

- Risk-Aligned Planning: Your investments match your comfort zone, not generic market recommendations

- Regular Reviews: Strategies adapt as your life evolves, ensuring your financial plan remains relevant

- Emotional Anchor: During market volatility, professional guidance helps you stay calm and confident, avoiding impulsive decisions

- Tax Optimization: Financial planning in India enables you to understand tax implications and maximize savings through strategic planning

Understanding the Growing Market Opportunity

India’s wealth management landscape is rapidly evolving. The country is expected to become the world’s fourth-largest economy by 2025, with the IMF projecting 6.5% growth for FY26. This economic momentum, combined with rising affluence and expanding middle class, creates unprecedented opportunities for wealth creation.

The demand for wealth management services in terms of assets under management (AUM) is expected to almost double, climbing from US$1.1 trillion in FY24 to US$2.3 trillion by FY29. This growth presents both opportunities and challenges for individual investors.

Smart Investment Tips for Beginners

If you’re just starting your investment journey in India, here are essential tips to guide you:

Define Your Investment Goals: Whether it’s retirement planning, children’s education, or buying a home, clear goals help determine your investment strategy and risk tolerance

Start Small and Stay Consistent: Regular investments through SIPs can help you benefit from rupee cost averaging and compound growth

Diversify Your Portfolio: Don’t put all your money in one type of investment. Spread risk across different asset classes

Understand Your Risk Appetite: Choose investments that align with your comfort level and time horizon

Stay Informed: Keep yourself updated about market trends and regulatory changes affecting your investments

FAQs on Wealth Management in India

Q. What is the first step in wealth management in India?

Start with defining your financial goals and build an emergency fund plus adequate insurance coverage before chasing returns.

Q. Is it safe to start investing in India with mutual funds?

Yes, when aligned with your risk appetite and reviewed regularly. SIPs are one of the safest and simplest starting points for beginners.

Q. Why should I choose a wealth manager instead of DIY investing?

A wealth manager helps with strategic planning, behavioral discipline, and avoiding emotional mistakes—ensuring your money stays on track for long-term success.

Q. How much should I invest as a beginner?

Start with what you can afford to invest regularly. Even ₹1,000 per month through SIPs can grow significantly over time due to compounding.

Q. What are the tax benefits of financial planning in India?

Financial planning helps you understand tax implications and optimize your investments through tax-saving instruments like ELSS.

Final Word: Wealth with Intent

The best way to start wealth management in India is not by chasing the next hot tip—it’s by starting with intent, building a foundation, and staying consistent.

According to a financial freedom survey by Scripbox, 80% of Indian investors are unsure of their retirement planning. This statistic underscores the critical importance of proper financial planning and professional guidance.

Your wealth journey doesn’t have to be complicated. With the right approach, it becomes a partnership—rooted in clarity, care, and purpose. Whether you choose to work with professional wealth managers or start your DIY journey, the key is to begin now and stay committed to your financial goals.

The Indian wealth management market is projected to reach $286.91 billion by 2030 with a CAGR of 10.96%. This growth creates immense opportunities for individual investors who start their wealth-building journey with proper planning and professional guidance.Remember, financial planning is not just about managing money—it’s about creating a roadmap for your dreams and ensuring financial security for you and your loved ones. Start today, stay consistent, and watch your wealth grow systematically over time.

Disclaimer

This article is intended solely for educational and informational purposes. It does not constitute investment advice, trading recommendations, or a solicitation to buy or sell any securities or financial instruments. The views expressed are based on publicly available data, regulatory studies, and industry observations, including reports published by the Securities and Exchange Board of India (SEBI). Readers are advised to assess their financial objectives, risk appetite, and suitability before making any investment or trading decisions. Derivatives trading, including Futures & Options (F&O), involves substantial risk and may not be suitable for all investors. Past performance is not indicative of future results. Investors should consult a SEBI-registered investment adviser or other qualified financial professional before acting on any information presented herein.