Money plans are built around goals. Retirement. Children’s education. A second home. Financial freedom.

But life has its own agenda.

Life insurance exists for one reason: to protect the people who depend on you if you are not there to provide for them. It is not an investment strategy but more of a financial shock absorber. And sometimes, that is the most powerful tool in a plan.

Let’s look at what it really does and why it deserves a serious place in your financial blueprint.

1. Protecting Your Family’s Lifestyle

When the earning member of a family is no longer there, the emotional vacuum is obvious. The financial vacuum is often underestimated.

A life insurance policy, especially a pure term plan, acts as an income replacement mechanism. If someone earns ₹15–20 lakh per year, the family’s lifestyle is structured around that cash flow. Rent or EMI, school fees, medical expenses, groceries, insurance premiums, domestic help, even annual vacations—these are not luxuries. They are routine commitments.

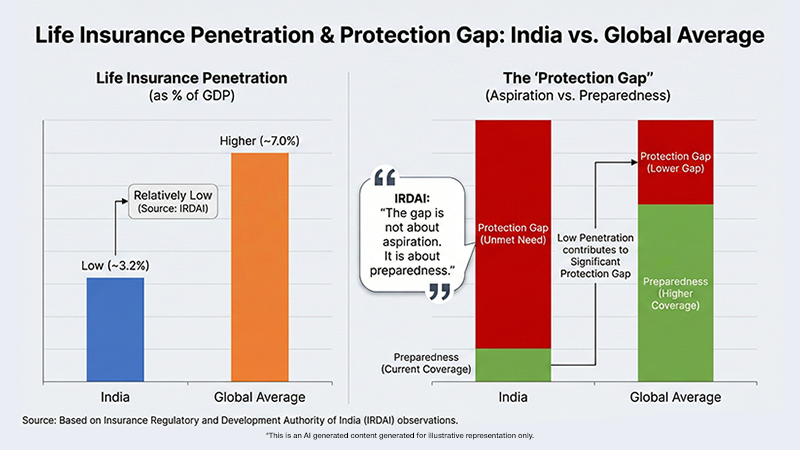

According to the Insurance Regulatory and Development Authority of India (IRDAI), life insurance penetration in India remains relatively low compared to global averages, highlighting a significant protection gap. The gap is not about aspiration. It is about preparedness.

A need based analysis is one of best ways to evaluate the amount of life cover required and it should cover the following:

- EMIs continue without stress

- Children’s education plans stay intact

- Household expenses run without disruption

- Long-term goals do not collapse overnight

Lifestyle protection is not about extravagance. It is about stability.

2. Financial Security Through a Lump Sum Payout

In the event of death during the policy term, life insurance pays a lump sum to the nominee. That single transfer of capital changes the trajectory of the family’s future.

Without it, the surviving spouse may face:

- Immediate liquidity stress

- Pressure to liquidate long-term investments

- Compromises in children’s education

- Dependency on extended family

With it, there is breathing space.

The Life Insurance Corporation of India (LIC) data consistently shows that claims settlement ratios remain high across established insurers, reflecting the industry’s core function—income protection.

The payout can be structured to:

- Create a corpus that generates regular income

- Clear outstanding loans

- Fund education milestones

- Support retirement needs of the surviving spouse

Life insurance does not remove grief. It removes financial panic.

3. Protecting Family Assets from Debt

Loans may help build a house, fund a business, or improve lifestyle, but they also create a financial obligation that survives the borrower. If the main earning member is no longer around, EMIs do not stop and lenders do not step back.

Without sufficient life insurance, families may have to liquidate investments or sell assets to repay debt. A well-designed term plan can prevent that outcome by providing funds to clear liabilities quickly and protect the family’s long-term financial stability.

In some cases, structuring the policy under the MWP Act can add another layer of protection by keeping the insurance proceeds earmarked for the wife and children, rather than exposing them to creditor claims. That is why insurance should be seen not only as income replacement, but as liability protection.

4. Low Cost, High Cover: The Term Plan Advantage

Here is the part many people underestimate.

A pure term insurance plan offers high coverage at a surprisingly affordable premium—especially when purchased early.

For a healthy individual in their 20s or 30s, a ₹1 crore cover can often cost less than what many people spend annually on dining out or subscription services. The exact premium varies by age, health, and insurer, but the principle is consistent: maximum protection at minimal cost.

Term insurance is simple:

- No maturity benefit

- No investment component

- Pure risk cover

Buying life insurance when young secures a lower long-term premium. The true value is the peace of mind it offers, not financial gain.

5. Tax Efficiency

Under Section 80C of the Income Tax Act, premiums paid toward life insurance are eligible for deduction within the prescribed limits.

Additionally, under Section 10(10D), the death benefit received by the nominee is generally exempt from tax, subject to prevailing conditions and policy compliance.

These provisions are governed by the Income Tax Department of India and are part of India’s broader framework encouraging long-term financial security.

Tax benefits should never be the sole reason to buy insurance. But when protection and tax efficiency align, it strengthens the overall financial structure.

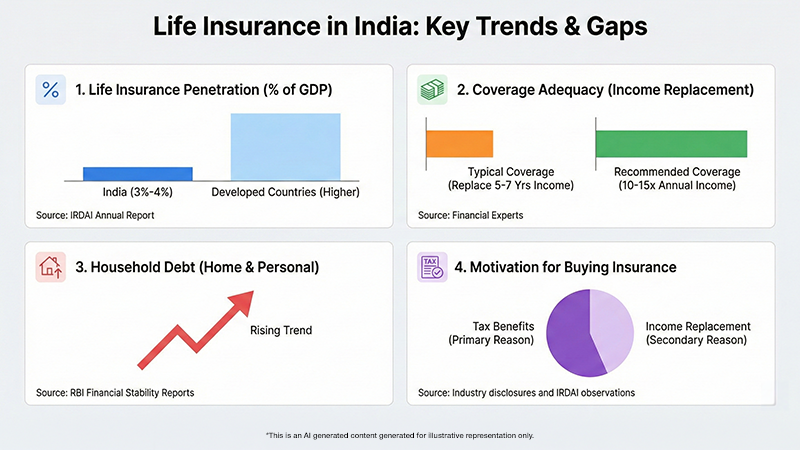

The Protection Gap: What the Data Says

• As per Insurance Regulatory and Development Authority of India Annual Report, life insurance penetration in India is currently around 3%–4% of GDP, which is lower than in many developed countries.

• Many insured individuals have insufficient coverage, meaning they can’t replace even 5–7 years of income. Financial experts suggest having coverage of at least 10–15 times your annual income, although this can depend on your obligations and life stage.

• Reserve Bank of India Financial Stability Reports states household debt in India is rising, indicating an increase in home and personal borrowing.

• Industry disclosures and IRDAI observations show that while awareness is improving, many people still buy insurance mainly for tax benefits rather than planning for income replacement.

What Does This Imply?

Most families are just one income shock away from financial strain.

Why You Should Consider It

Life insurance is not a product for everyone. If no one depends on your income, the urgency is low.

But if:

- Your family relies on your earnings

- You have ongoing EMIs

- You are building long-term goals for children

- You want financial continuity even in your absence

Then insurance is not optional anymore!

Financial planning is often about growth—equity, compounding, asset allocation. But planning also requires acknowledging risk.

We insure cars that depreciate.

We insure phones that become obsolete.

Yet many families remain uninsured against the loss of their primary income source.

Protect What Matters Most: How SubhShanti Wealth Secures Your Family’s Financial Future

At SubhShanti Wealth, we handle life insurance with clarity and responsibility. Our focus is on assessing risk and understanding your family’s financial needs to create effective coverage. We aim to simplify complexities and align your protection strategy with your income, liabilities, and long-term goals.

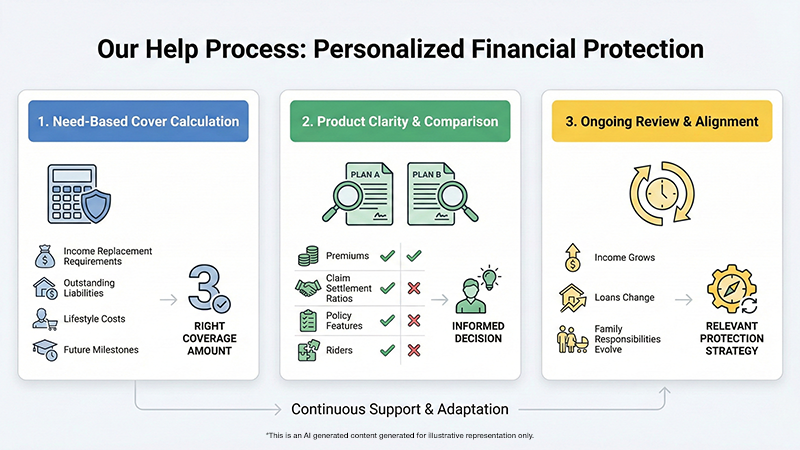

Here’s how we help:

- Need-Based Cover Calculation

We assess income replacement requirements, outstanding liabilities, lifestyle costs, and future milestones to determine the right coverage amount — not an arbitrary number. - Product Clarity & Comparison

We help you evaluate term plans transparently — premiums, claim settlement ratios, policy features, riders — so your decision is informed, not emotional. - Ongoing Review & Alignment

As income grows, loans change, or family responsibilities evolve, we review and recalibrate your protection strategy to keep it relevant.

If financial security for your family is a priority, it deserves a structured conversation.

Get in touch with SubhShanti Wealth today — and build a protection plan that stands firm, even when life doesn’t.