Tired of juggling countless investment tips, market whispers, and tax rules that change faster than the traffic light? You’re not alone. Across India, busy professionals and growing families are discovering that handing the reins to seasoned investment experts can turn financial chaos into calm, goal-driven progress. Before you leap, though, there are a few smart moves that separate confident wealth builders from anxious guessers.

In this comprehensive guide, we unpack those moves—step by step—so you can decide if outsourcing your investments is the power play your money deserves.

Understanding Outsourced Investment Services in India

Outsourced investment services involve delegating your portfolio management to external financial experts or firms. In India, this typically includes Portfolio Management Services (PMS), wealth management companies, and investment management firms that handle everything from asset allocation to risk management and ongoing portfolio monitoring.

The Indian investment services industry has grown tremendously, with assets under management reaching new heights each year. This growth reflects increasing investor ease and recognition of the value professional expertise brings to investment outcomes.

When you outsource your investments in India, you gain access to seasoned professionals who understand local market dynamics, regulatory requirements, and investment opportunities specific to the Indian economy.

These services range from basic investment advice to comprehensive wealth management solutions. Professional investment experts have access to research tools, market data, and analytical resources that individual investors might find expensive or time-consuming to utilize effectively. They also bring experience managing money through different market cycles, including the volatile periods that characterize emerging markets like India.

The regulatory framework in India, overseen by the Securities and Exchange Board of India (SEBI), ensures that outsourced investment services maintain high standards of transparency, compliance, and investor protection. This regulatory oversight provides an additional layer of security for investors considering professional investment management services.

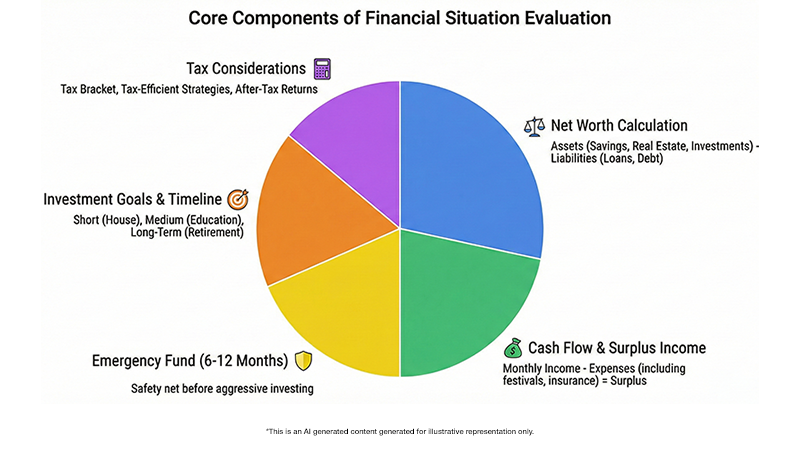

Evaluate Your Current Financial Situation

Before engaging any outsourced investment service in India, conduct a thorough assessment of your financial position. This evaluation forms the foundation of any successful investment strategy and helps you communicate effectively with potential service providers.

Start by calculating your net worth, including all assets such as savings accounts, fixed deposits, real estate, existing mutual fund investments, Employee Provident Fund (EPF), Public Provident Fund (PPF), and any other investments. Simultaneously, list all liabilities including home loans, personal loans, credit card debt, and other outstanding obligations. This complete picture helps determine how much you can realistically allocate to professional investment management.

Consider your cash flow patterns by analyzing your monthly income and expenses. Factor in India-specific expenses like annual insurance premiums, children’s education costs, and festival-related expenses. Identify how much surplus income you have available for investments after covering essential expenses and maintaining an adequate emergency fund. Financial experts recommend having six to twelve months of expenses saved as an emergency fund before focusing on aggressive investment strategies.

Your investment timeline is crucial in the Indian context, where many investors have multiple financial goals with different timelines. Are you saving for a house down payment in three years, planning for your children’s higher education in ten years, or building wealth for retirement in twenty-five years? Different timeframes require different investment approaches, and professional investment experts can help align your portfolio with these varied objectives.

Tax considerations are particularly important in India, where different investment products have varying tax implications. Understanding your current tax bracket and potential future tax situation helps investment experts recommend tax-efficient investment strategies that maximize your after-tax returns.

Define Your Investment Goals and Risk Tolerance

Clear, specific investment goals are essential for successful outsourcing in India’s diverse investment landscape. Vague objectives like “making money” don’t provide sufficient direction for professional managers to create appropriate strategies. Instead, establish concrete, measurable goals with specific timelines that reflect Indian market realities.

Consider categorizing your goals by priority and timeline. Primary goals might include retirement planning, children’s education funding, or wealth preservation, while secondary goals could involve purchasing a vacation home or funding international travel. Each goal may require different investment approaches, considering factors like inflation in India, currency fluctuation, and sector-specific growth opportunities. Even highly accomplished professionals often misjudge their true risk tolerance or delegation strategy—a pattern we’ve examined in our article 3 Things Most CXOs Get Wrong About Wealth.

Risk tolerance in the Indian context encompasses both your ability and willingness to accept investment losses. Your ability to take risk depends on factors like your age, income stability, job security, existing savings, and family responsibilities. Someone with decades until retirement and stable employment in a growing sector can typically weather market volatility better than someone approaching retirement with limited savings.

Your willingness to take risk is psychological and relates to how comfortable you feel watching your investments fluctuate. Indian markets can be particularly volatile, with significant swings during election periods, monsoon seasons, and global economic events. Some investors sleep soundly knowing their portfolios might decline 20% in a bad year, while others lose sleep over 5% fluctuations.

Consider India-specific risk factors such as regulatory changes, currency depreciation, and sector-specific risks in rapidly evolving industries like technology and pharmaceuticals.

Document your goals and risk tolerance clearly. This documentation becomes invaluable when communicating with potential service providers and serves as a reference point for evaluating whether their proposed strategies align with your objectives and the unique aspects of investing in India.

Research Different Types of Service Providers in India

The Indian investment services landscape includes various types of providers, each with distinct approaches, fee structures, and service levels.

- Portfolio Management Services (PMS) – popular among high-net-worth individuals, typically minimum ₹50 lakhs, offering personalized strategies and direct ownership.

- Wealth management companies – comprehensive, for ultra-high-net-worth individuals, starting ₹1 crore+.

- Mutual fund companies with advisory services – lower minimums (₹5–50 lakhs).

- Independent experts and boutique firms – sector-specific focus (tech, pharma, infra).

- Robo-advisory platforms – emerging, algorithm-driven, low-cost.

- Bank-affiliated investment services – convenient but may present conflicts of interest.

Understand Fee Structures and Costs in India

Investment fees significantly impact your long-term returns.

- PMS fees: 1%–3% annually, plus performance fees (10%–25% of profits above benchmarks).

- Wealth management fees: 1%–2.5% annually.

- Transaction costs: brokerage fees, STT, GST, and other statutory charges.

- Tax implications: management fees may be deductible, performance fees usually are not.

Even a 1% fee difference on a ₹50 lakh portfolio can compound to over ₹10 lakhs in 20 years at 10% annual returns.

Check Credentials and Regulatory Compliance

The industry includes many qualified professionals but also some without proper credentials.

- Verify certifications: Certified Financial Planner (CFP), Chartered Financial Analyst (CFA).

- Ensure SEBI registration and regulatory compliance.

- Look for proven track records through crises like demonetisation, 2020 pandemic.

- Evaluate against Nifty 50, Nifty 500, or sector indices.

- Review client testimonials and case studies.

Understand Service Models and Communication

Different service providers in India offer varying models:

- Communication frequency – quarterly reviews, digital updates, apps.

- Reporting standards – real-time access, performance reporting, tax docs.

- Discretionary vs. Non-discretionary models – convenience vs. control.

- Scope – pure investment management vs. full wealth management.

- Transparency – rationale, reviews, attribution analysis.

Prepare Questions for Initial Consultations

Ask about:

- Investment philosophy – portfolio construction, asset allocation, sector strategies.

- Performance & benchmarks – how they measure success, crisis management.

- Tax efficiency – capital gains harvesting, tax-saving vs. growth.

- Risk management – downturn strategies, diversification.

- Client service – responsiveness, retention, reporting.

- Regulatory compliance – SEBI status, ethical standards.

Start Small and Test the Waters

- Begin with a smaller allocation.

- Compare results vs. mutual funds or direct equities.

- Track performance over different market cycles.

- Set clear evaluation criteria: communication, performance, reporting, tax efficiency.

- Document positive and negative experiences.

Several investors discover—often too late—that the wrong service model or expert choice can create structural inefficiencies, many of which are highlighted in Common Mistakes HNIs Should Avoid When It Comes to Wealth Planning.

SubhShanti Wealth—Your Financial Co-Pilot for the Market Swings!

In a world where market fluctuations and policy announcements can create uncertainty, SubhShanti Wealth offers a steady hand.

We are more than just analysts; we are experienced navigators who have successfully weathered major market events, from demonetisation to the pandemic. Our decades of experience inform every decision we make for you.

Our approach goes beyond market expertise. We build bespoke investment roadmaps based on your unique circumstances, family needs, and tax situation.

Transparency is a cornerstone of our service, with clear explanations, a secure app offering 24/7 visibility, and quarterly reports explaining every move.

While technology powers thorough research operations, human expertise drives decisions. During volatility, you’ll consult a dedicated investment expert who knows your financial story.

Our fee structure is transparent, upfront, and aligned with industry standards.

Whether you’re a new investor or an experienced wealth creator, SubhShanti Wealth combines market intelligence, human insight, and clarity to help achieve your goals.

Making the Right Choice for Your Financial Future

The decision to outsource investment management is a significant step.

Success depends on the right match:

- Trust, transparency, and communication.

- Alignment of philosophy and objectives.

- Long-term focus on tax efficiency, risk management, and systematic wealth building.

By following these guidelines and conducting thorough due diligence, you can make an informed decision that secures your financial future.

The right investment expert can help you navigate India’s markets, optimize tax efficiency, and build systematic wealth toward achieving your life goals.Ready to embark on a journey toward financial tranquility and clear direction? Let’s chart your course—together.

Disclaimer

This article is intended solely for educational and informational purposes. It does not constitute investment advice, trading recommendations, or a solicitation to buy or sell any securities or financial instruments. The views expressed are based on publicly available data, regulatory studies, and industry observations, including reports published by the Securities and Exchange Board of India (SEBI). Readers are advised to assess their financial objectives, risk appetite, and suitability before making any investment or trading decisions. Derivatives trading, including Futures & Options (F&O), involves substantial risk and may not be suitable for all investors. Past performance is not indicative of future results. Investors should consult a SEBI-registered investment adviser or other qualified financial professional before acting on any information presented herein.