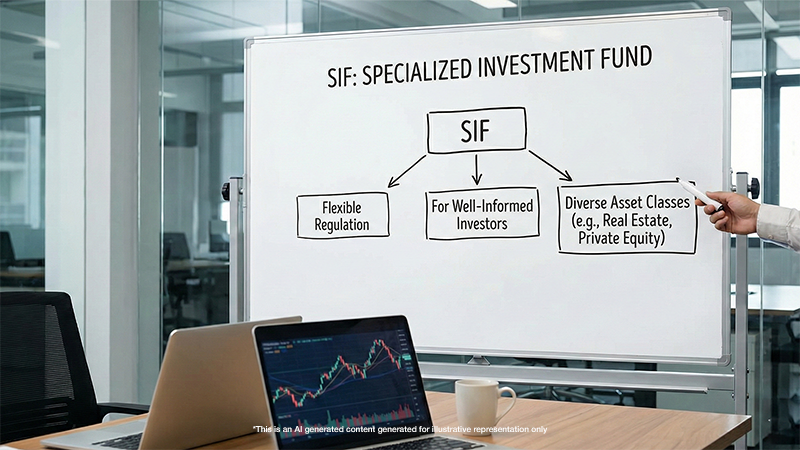

What is SIF?

Specialised Investment Funds (SIFs) are a new, SEBI-regulated investment category introduced in India that fills the gap between traditional mutual funds and more complex portfolio management services (PMS) or alternative investment funds (AIFs). They target high-net-worth investors with a minimum ₹10 lakh investment, offering advanced, strategy-driven approaches not typical of mutual funds.

SIFs allow fund managers to invest in strong opportunities while also protecting portfolios during difficult phases. They can adjust where money is invested as market trends change, spread investments across multiple asset types for balance, and use protective tools to reduce the impact of sharp market swings. The goal is smarter risk management and smoother outcomes over full market cycles.

Unlike traditional mutual funds, which usually stay fully invested and depend mainly on rising prices, SIFs can actively manage both growth and downside risks within clearly defined limits.

SIFs also come in different structures to suit different investor needs. Some allow investors to enter or exit freely, making them suitable for those who prefer flexibility. Others offer exits only at fixed intervals, ideal for investors who are comfortable staying invested for a defined period. There are also options where money is committed for a fixed term, best suited for investors who can stay patient and allow the strategy time to work without short-term pressures.

All SIFs operate under SEBI’s regulatory framework, following mutual fund rules along with additional safeguards specific to these strategies. This ensures transparency, discipline, and investor protection, while still allowing enough flexibility to navigate markets more effectively

Who Can Invest ?

- You must invest ₹10 lakh in total to participate in a SIF (per PAN, per SIF).

- You can reach this ₹10 lakh in one go or gradually — there’s no time limit.

- Accredited investors as defined by SEBI, who usually have:

- High income (₹2 crore or more a year), or

- High net worth (₹7.5 crore or more, with a large part in financial assets), or

- A mix of both income and net worth

They are not required to follow the minimum investment rule.

- You can use SIP, SWP, or STP within a SIF, but your total investment must still add up to ₹10 lakh unless you’re accredited.

SIFs: Benefits vs. Risks

| Benefits | Risks |

| Higher return potential through tactical asset allocation | Market Risk: Values fluctuate with equity, debt, and commodity movements. |

| Hedging capabilities for downside protection | Leverage Risk: Borrowing/derivatives can amplify losses. |

| Tax efficiency similar to mutual funds | Short Selling Risk: Losses can escalate if markets move against short positions. |

| Access to unique sectors like private equity, commodities, real estate | Liquidity Risk: Complex or illiquid assets may delay withdrawals. |

| Professional, strategy-driven fund management | Strategy Risk: Outcomes depend on fund manager calls. |

| Regulatory safeguards improving trust and transparency | Regulatory Risk: Changes in SEBI rules or taxation can impact operations. |

However, products like SIFs deliver their true value only when used with discipline. As explained in “Rebalancing: The Understated Discipline That Keeps Portfolios Healthy,” strategies that dynamically adjust exposure across market cycles play a crucial role in protecting portfolios—and SIFs are designed to support exactly that kind of structured rebalancing.

Comparing SIFs and Traditional Mutual Funds

| Feature | Specialized Investment Funds (SIFs) | Traditional Mutual Funds |

| Investor Eligibility | ₹10 lakh minimum (exempt for accredited investors) | Open to all, low minimum (₹100-₹500) |

| Investment Strategy | Long-short, sector rotation, tactical asset allocation | Primarily long-only in equity/debt |

| Liquidity | Variable: daily to periodic redemptions | Generally daily liquidity |

| Risk Profile | Generally higher (due to leverage, shorting) | Ranges from low to very high |

| Tax Treatment | Taxed like mutual funds (advantageous) | Standard mutual fund taxation |

As discussed in “Top Alternative Investments in High-Value Portfolios: Unlocking Potential with PMS, AIF, and SIF,” investors today are increasingly looking beyond traditional mutual funds. SIFs stand out in this landscape by offering advanced strategies with regulatory comfort—making them a practical middle ground for sophisticated portfolios.

SIF Categories

SEBI Specialized Investment Funds (SIFs) are primarily categorized into three main types:

Equity-Oriented SIFs

1. Equity Long–Short Fund

- Mostly invests in stocks (80% or more).

- Can also take limited negative bets (up to 25%) if the manager expects some stocks to fall.

2. Equity Ex-Top 100 Long–Short Fund

- Focuses mainly on mid- and small-sized companies (outside the top 100).

- Can take small negative positions (up to 25%) in select stocks when needed.

3. Sector Rotation Long–Short Fund

- Invests in up to 4 sectors at a time—like IT, banking, pharma, etc.

- Switches between sectors depending on which ones look strong.

Debt-Oriented SIFs

4. Debt Long–Short Fund

- Invests in bonds and fixed-income products.

- Can also take negative or protective positions to manage risk and benefit from interest rate moves.

5. Sectoral Long–Short Debt Fund

- Invests in debt across at least two different sectors—like banking, energy, manufacturing, etc.

- Designed to capture opportunities or manage risks across sectors.

Hybrid SIFs

6. Active Asset Allocator Long–Short Fund

- Spreads money dynamically across different asset classes—equity, debt, gold, REITs, etc.—based on market conditions.

- Provides flexibility by shifting between assets as the market changes.

7. Hybrid Long–Short Fund

- Keeps a balanced mix, with at least 25% in equity and 25% in debt always.

- Can take limited negative positions to manage risk or enhance returns.

How SIF Returns Are Taxed

| SIF Type | Holding Period | Gain Type | Tax Rate |

| Equity-oriented (65%+ in equities) | ≤ 12 months | Short-Term Capital Gains (STCG) | 20% |

| Equity-oriented (65%+ in equities) | > 12 months | Long-Term Capital Gains (LTCG) | 12.5% |

| Debt SIF | ≤ 24 months | Short-Term Capital Gains (STCG) | As per individual tax slab |

| Debt SIF | > 24 months | Long-Term Capital Gains (LTCG) | As per Tax Slab |

| Hybrid SIF (equity exposure < 65%) | ≤ 24 months | Short-Term Capital Gains (STCG) | As per individual tax slab |

| Hybrid SIF (equity exposure < 65%) | > 24 months | Long-Term Capital Gains (LTCG) | 12.5% without indexation |

It still makes sense to check with your tax expert to optimise taxation for your personal situation.

If this prospect excites you, explore our other blogs to discover the further benefits mutual funds offer : Things You Didn’t Know Mutual Funds Could Do (But They Can or explore SIPs to build lasting wealth!

How SubhShanti Wealth Can Assist in Your SIF Journey

SubhShanti Wealth offers comprehensive, expert support tailored for investors interested in SIFs. Their guidance can be broken down into clear points:

- Personalized Assessment: Evaluate if SIFs align with the investor’s roadmap, risk tolerance, and investment horizon.

- Strategy Selection: Help choose the most suitable SIF strategies (like long-short equity, sector rotation) based on market outlook and individual preferences.

- Tax Optimization: Explain tax implications of SIF returns and suggest tax-efficient investment approaches.

- Portfolio Integration: Guide on how to integrate SIFs into the broader investment portfolio to achieve diversification and risk management.

- Regular Monitoring: Provide ongoing portfolio reviews and performance tracking to keep investments aligned with the roadmap.

- Education and Transparency: Ensure investors understand the complex strategies involved in SIFs through clear communication and education.

- Regulatory Compliance: Assist in meeting all SEBI requirements and paperwork related to SIF investments.

- Tailored Solutions: Offer customized financial plans incorporating SIFs along with other instruments to optimize wealth creation and financial security.

SubhShanti Wealth’s experienced experts bring deep knowledge and personalized attention, making sophisticated products like SIFs accessible and manageable for their clients aiming for long-term financial success.

For many investors, this combination—professional management, strategy flexibility, and tax efficiency—makes SIFs a smart middle ground between traditional mutual funds and complex high-minimum products.

SIF : Top 3 Things Investors Ask!

1. How does the NAV cut-off work? To get today’s NAV, both application and funds must reach before 3 PM. After that, the next business day’s NAV applies.

2. How does Redemption work?

Redemptions happen once a month on the first working day. Before 3 PM = same-day NAV; after 3 PM = next month’s NAV.

3. What are the minimum investment requirements?

You must maintain ₹10 lakh at PAN level. If your value drops below this, only full redemption is allowed—no partial withdrawals.

Final Word

SIFs are steadily emerging as a meaningful choice for Indian investors, with industry experts projecting the category could grow to nearly ₹15,000 crore in the coming years — driven by rising demand for smarter, more tax-efficient investment options. They sit between regular mutual funds and high-ticket products like PMS or AIFs, offering flexible strategies, better risk management tools, and favourable taxation—all within SEBI’s regulated framework. For many investors, SIFs can be a practical way to add strength and stability to their long-term portfolio without taking on the complexity or cost of advanced products.

Disclaimer

This article is intended solely for educational and informational purposes. It does not constitute investment advice, trading recommendations, or a solicitation to buy or sell any securities or financial instruments. The views expressed are based on publicly available data, regulatory studies, and industry observations, including reports published by the Securities and Exchange Board of India (SEBI). Readers are advised to assess their financial objectives, risk appetite, and suitability before making any investment or trading decisions. Derivatives trading, including Futures & Options (F&O), involves substantial risk and may not be suitable for all investors. Past performance is not indicative of future results. Investors should consult a SEBI-registered investment adviser or other qualified financial professional before acting on any information presented herein.