Most investors pick funds by looking at star ratings or last year’s returns. Here is what a well-trained distributor actually checks before recommending any scheme to you.

Every week, someone walks into a mutual fund distributor’s office holding a printout from a financial website. On it are five or six fund names, all marked with five stars, all showing returns that look breathtaking over a one-year or three-year period. The person sits down and says, “I want to invest in these.”

The distributor’s job at that moment is not to say yes. It is to ask the right questions — and to look at the right numbers.

The difference between a distributor who helps you build real wealth and one who simply processes your paperwork is this: the good one has a framework for evaluating a fund that goes far deeper than any rating website. They look at rolling returns, risk-adjusted metrics, consistency, expense ratios, fund manager track records, and a dozen other things that never show up in those printouts.

This article walks you through that framework, step by step. By the end, you will understand how a serious distributor evaluates a mutual fund scheme — and you will be better equipped to ask the right questions yourself.

Why Star Ratings Alone Will Mislead You

Let us start with something that will surprise you. Star ratings given by fund rating agencies whether they are Morningstar, Value Research, or any other are calculated using past performance data. They are backward-looking by design. A fund that earned five stars last year may have done so because its category happened to perform well, not because the fund itself made exceptional decisions.

There is nothing wrong with using ratings as a starting point. But if a distributor stops there, they are doing their client a serious disservice.

Consider what happens in a market cycle. Small-cap funds tend to look brilliant during bull runs. Their three-year returns can easily cross 30–35%. They get five stars. Investors pile in. Then the market corrects, and the same funds fall 40–50% while large-cap funds fall 15–20%. The star rating was real — but it told you about a past that no longer existed.

“A star rating tells you where the fund has been. A good distributor tells you where the fund is likely to go and whether you can handle the journey.”

A trained distributor knows this. So instead of only asking “how has this fund performed,” they ask “how has this fund performed across different market conditions” and that question leads to a completely different set of metrics.

Rolling Returns vs. Point-to-Point Returns

This is probably the most important distinction in mutual fund selection, and the one most retail investors never encounter.

When a website shows you that a fund gave 24% returns over three years, it is showing you a point-to-point number. It took the NAV on one specific date three years ago and compares it to the NAV today. Change either date by a few months and the number can look completely different.

Rolling returns solve this problem. Instead of picking two arbitrary dates, you calculate the fund’s three-year return starting from every single day over the past five or seven years. You then look at the distribution of those returns.

→ What percentage of three-year periods gave positive returns? A strong fund should show positive three-year rolling returns more than 90% of the time.

→ What was the median three-year rolling return? This is a truer picture of what an average investor actually experienced.

→ What was the worst three-year rolling return? This tells you about downside risk over a realistic holding period.

→ How consistent was performance across different periods? A fund that gives 28% sometimes and 4% other times is very different from one that consistently gives 14–16%.

A good distributor will pull up rolling return data from databases that track this — and they will compare the fund to both its benchmark index and its category peers on the same basis. A fund that consistently beats its benchmark across rolling periods, rather than just in one lucky stretch, is a genuinely strong performer.

| WHAT TO ASK YOUR DISTRIBUTORAsk them to show you the fund’s three-year rolling returns over the past seven years. If they cannot produce this data or seem unfamiliar with the concept, that itself tells you something important about the quality of their analysis. |

The Sharpe Ratio — Getting Paid for Risk

Imagine two funds. Fund A gives 16% annual returns. Fund B also gives 16%. On the surface they look identical. But Fund A’s portfolio swings wildly — it dropped 38% during one downturn before recovering. Fund B fell only 18% in the same period before recovering to the same level. Which fund is actually better?

Fund B. Clearly. Because it gave you the same return with significantly less pain.

The Sharpe ratio captures this. It measures how much return a fund earns per unit of risk taken. The formula uses the fund’s excess returns over a risk-free rate (typically the prevailing repo rate or government security yield) divided by its standard deviation — which is a measure of how much the fund’s returns fluctuate.

A higher Sharpe ratio means the fund is generating more return for every unit of risk it takes on. Two funds with the same returns but different Sharpe ratios are not equally good — the one with the higher ratio is the better risk-adjusted performer.

One thing to keep in mind: Sharpe ratios should always be compared within the same category. A liquid fund’s Sharpe ratio and an equity fund’s Sharpe ratio are not comparable. When a distributor uses the Sharpe ratio, they compare a fund only to its direct peers — other flexi-cap funds, other mid-cap funds, and so on.

Alpha and Beta — Separating Skill from Market Movement

Every mutual fund participates in market movements to some degree. When the Nifty 50 rises 10%, most large-cap funds will also rise — not because the fund manager did anything clever, but simply because the market went up. This is called beta exposure.

Alpha is what is left over after accounting for that market movement. It represents the fund manager’s genuine contribution — the return they generated through stock selection, sector calls, and portfolio construction that cannot be attributed simply to the market going up.

A positive alpha means the fund is consistently beating what the market would predict it should earn given its level of market exposure. A negative alpha means the fund is underperforming — even after accounting for its market risk profile.

Beta, meanwhile, tells you how much the fund moves relative to its benchmark. A beta of 1.2 means the fund tends to rise 12% when the market rises 10%, but also falls 12% when the market falls 10%. A beta of 0.8 means it is more defensive — it captures less of the upside but also less of the downside.

A distributor uses alpha and beta together. For an aggressive investor looking for higher growth, a fund with high beta and positive alpha makes sense. For a conservative investor or someone nearing a financial goal, a fund with lower beta and still-positive alpha is more appropriate.

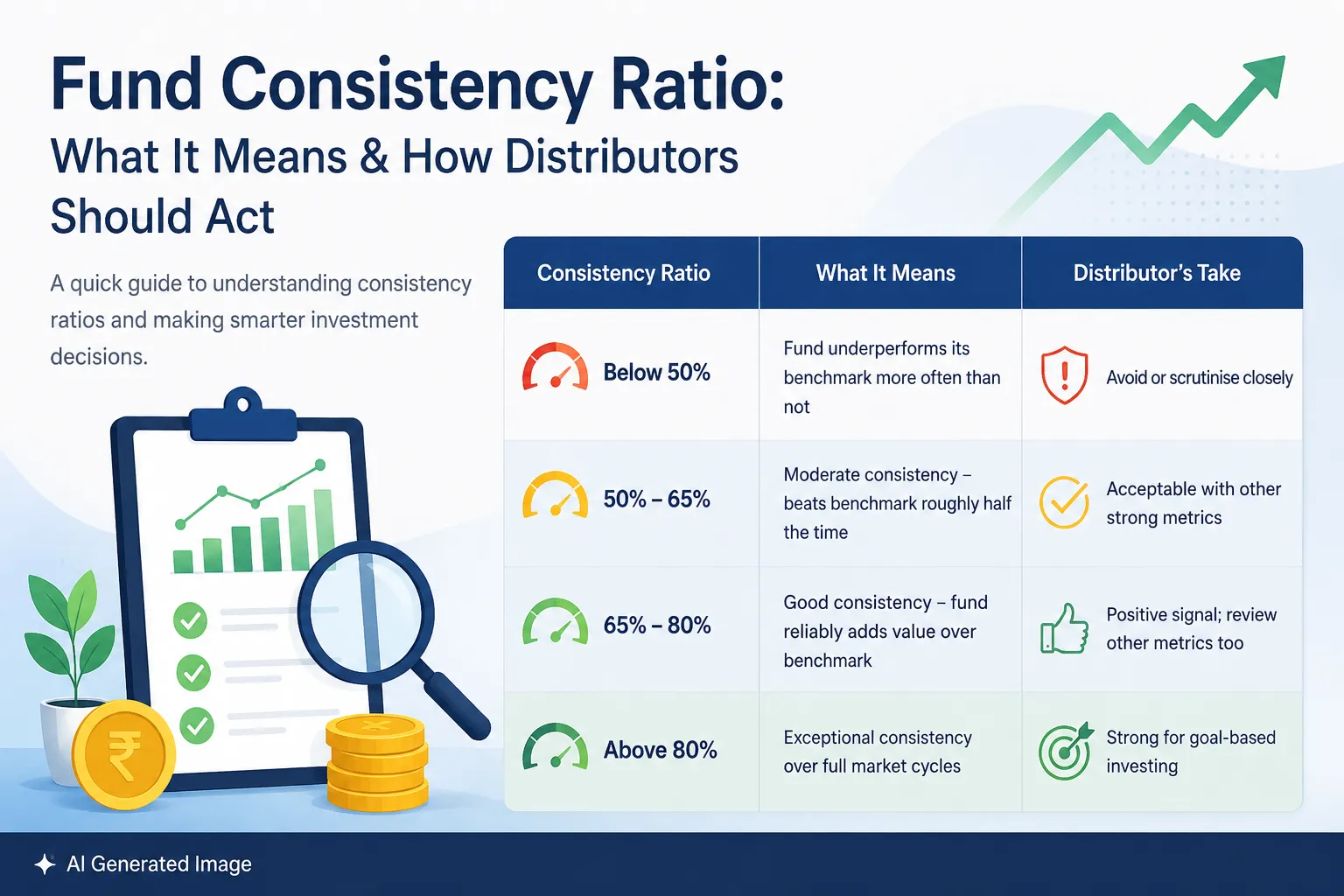

Consistency Ratio — The Metric Most People Have Never Heard Of

Rolling returns tell you what the fund earned over different periods. The consistency ratio tells you how often the fund actually beat its benchmark across those periods.

It is a straightforward calculation: out of all the measured rolling periods (say, three-year periods measured every month over seven years), what percentage of them did the fund beat its benchmark? A fund with a 65% or higher consistency ratio is genuinely outperforming — not just in one lucky window, but across the majority of measured periods.

A fund that beat its benchmark 90% of rolling periods is a more reliable performer than one that beat it 50% of the time, even if the latter occasionally produced spectacular returns. The consistent outperformer is one you can actually count on when you set a financial goal with a specific date attached to it.

Expense Ratio

Every mutual fund has an expense ratio (TER), which is the cost of accessing professional fund management, research capabilities, risk monitoring, regulatory compliance, technology infrastructure, and investor servicing. In many ways, it is the fee that keeps the investment ecosystem running and enables professionals to manage investors’ money on an ongoing basis.

For example, if a fund generates a gross return of 12% in a year and has an expense ratio of 1.8%, the investor receives a net return of 10.2%. While the expense ratio is deducted from returns, it also funds the expertise, processes, and resources that help the fund pursue those returns in the first place.

Importantly, expense ratios are not arbitrary. SEBI prescribes maximum TER limits based on a fund’s assets under management (AUM). As a scheme grows larger, the TER must decline within the regulatory framework, ensuring that investors benefit from economies of scale.

When comparing mutual funds, cost deserves attention but it should not be viewed in isolation. A lower expense ratio does not automatically make a fund superior, just as a higher expense ratio does not automatically make it expensive. The more relevant question is whether investors are receiving adequate value for the cost they are paying.

A good distributor helps investors evaluate this balance by examining the fund’s investment process, consistency, risk management framework, portfolio construction, and overall suitability for their financial goals. They also monitor whether a fund’s TER remains reasonable relative to regulatory limits and comparable funds within the same category.

Ultimately, successful investing is rarely about choosing the cheapest option. It is about identifying the combination of cost, quality, discipline, and long-term value that best supports an investor’s objectives.

| REGULAR PLAN VS. DIRECT PLAN — A WORD OF CLARITY One of the key reasons regular plans have higher expense ratios than direct plans is that they include compensation for the distributor’s services. Direct plans, on the other hand, have lower TERs because investors transact directly with the fund house and do not pay for advisory or distribution support through the fund.This difference in cost often leads investors to focus solely on the TER gap. However, the more important question is what an investor receives in return for that additional cost.Investing is not merely about selecting a mutual fund. It involves asset allocation, portfolio construction, risk assessment, goal mapping, behavioural coaching during market volatility, periodic reviews, rebalancing decisions, tax considerations, and staying disciplined through changing market cycles. For many investors, these activities can be difficult to manage consistently alongside their professional and personal responsibilities.Money management is effectively a full-time discipline. Some investors have the interest, knowledge, and time to manage their portfolios independently, making direct plans a suitable choice for them. Others prefer professional guidance to help navigate financial decisions, avoid common behavioural mistakes, and maintain a structured long-term investment approach. For such investors, the additional cost of a regular plan may represent payment for expertise, guidance, and ongoing support rather than simply an extra charge.Neither option is inherently better. The right choice depends on the investor’s knowledge, confidence, available time, and desire for professional assistance.To ensure transparency, SEBI requires distributors to disclose the commissions they receive. A trustworthy distributor discusses these costs openly, explains the services they provide in return, and enables investors to make an informed decision about whether those services justify the cost. |

Fund Manager Tenure and Track Record

A mutual fund’s past performance belongs to whoever managed it during that period. If the fund manager changed eighteen months ago, the five-year performance data you are looking at may have little to do with the person currently making the decisions.

This is something that rarely gets flagged on rating websites, but a careful distributor checks it every time.

They look at how long the current fund manager has been in the role. They also look at the manager’s track record across other funds they have managed — not just the one being evaluated. A manager who has delivered consistent risk-adjusted performance across different fund mandates is more reliable than one who has had one spectacular run in a single fund.

→ How many years has the current manager been managing this specific fund? Ideally three or more years to have a meaningful track record in this role.

→ What other funds does this manager handle? If they manage ten funds simultaneously, how much bandwidth do they actually have for each?

→ What was the fund’s performance before this manager took over? If current returns are high but the manager joined recently, that credit belongs to the previous manager.

→ What is the fund house’s track record for retaining talented managers? High attrition in a fund house’s investment team is a red flag.

AUM Size — When Too Big Becomes a Problem

Assets Under Management (AUM) reflects how much money investors have put into a fund. A larger AUM is not always better. For mid-cap and small-cap funds especially, very large AUM creates a problem: the manager cannot easily buy or sell large quantities of smaller stocks without moving the price against themselves.

A mid-cap fund with Rs. 25,000 crore in AUM faces structural difficulty deploying money into genuinely good mid-cap opportunities. The fund may end up drifting toward large-cap stocks just because those are the only ones liquid enough to absorb that much money — defeating the entire purpose of a mid-cap allocation.

For large-cap funds, this concern is less acute. For small and mid-cap funds, a good distributor pays close attention to AUM growth and compares it to the investable universe in that segment.

Portfolio Concentration and Overlap

A mutual fund’s portfolio — the list of stocks or bonds it holds — tells you a great deal about the manager’s conviction and investment style. A distributor examines this carefully.

High concentration (the top 10 holdings making up 60–70% of the portfolio) signals strong conviction and focused bets. This can amplify both gains and losses. Lower concentration means wider diversification, typically with lower volatility but also lower potential for significant outperformance.

Portfolio overlap is equally important when you hold multiple funds. If two funds in your portfolio hold the same 15–20 stocks, you are not getting the diversification you think you are. A good distributor analyses overlap across your entire portfolio — not just individual funds in isolation — and recommends combinations that genuinely spread your risk across different stocks, sectors, and styles.

Analyzing Market Cap Bias and Sectoral Allocation

Within an equity fund’s mandate, the manager makes active choices about which sectors to overweight or underweight relative to the benchmark. A fund that is overweight in banking and financial services when the sector does well will look brilliant. The same fund will look terrible when the sector corrects.

A distributor looks at whether the fund’s sectoral bets are consistent over time or whether the manager chases whatever sector recently performed. Consistent positioning, even if it underperforms briefly, is a better sign than a portfolio that changes completely based on recent momentum.

Similarly, many flexi-cap funds advertise the freedom to move between large, mid, and small-cap stocks. A distributor checks where the fund actually sits most of the time. A fund that calls itself flexi-cap but always stays 90% in large-caps is effectively a large-cap fund — not wrong, but you should know that before investing.

Note: The metrics discussed so far offer only a glimpse into the depth of fund evaluation. Behind every well-considered recommendation lies a much broader assessment framework, with an MFD examining multiple qualitative and quantitative factors before arriving at a decision.

How This Builds Credibility for a Distributor

You may wonder why a distributor would go through all this trouble when they could simply show you the top performers and collect their commission. The answer lies in what good practice looks like over a ten or fifteen year relationship with clients.

The mutual fund distribution business is built on long-term relationships. Investors may stay with the same experts for years, increase their investments over time, and rely on them through multiple market cycles. As a result, a distributor has a strong incentive to recommend funds that are suitable for the investor rather than simply chasing what is popular at the moment. Sustainable client outcomes build trust, and trust is what drives long-term growth for both the investor and the distributor.

In many ways, a distributor’s reputation is a reflection of the quality of decisions they help investors make.

AMFI’s code of conduct requires distributors to act in the investor’s best interest, to disclose all material information including their commissions, and to match fund recommendations to the investor’s stated risk profile and financial goals. A distributor who uses the analytical framework described in this article is not just doing good analysis — they are fulfilling their regulatory obligation.

| AMFI NOTE: All mutual fund distributors in India must be registered with AMFI and hold a valid NISM Series V-A certification. You can verify your distributor’s registration on the AMFI website at amfiindia.com. If a distributor cannot show you their ARN (AMFI Registration Number), do not invest through them. |

The Full Framework — What to Ask Your Distributor

Bringing everything together, here is a complete checklist of what a well-prepared distributor should be able to discuss with you before recommending any fund:

→ Rolling returns over three-year and five-year periods, measured across the last seven to ten years — not just point-to-point returns from one date to another.

→ Sharpe ratio compared to category peers, showing how much return the fund generates per unit of risk, and how that compares to alternatives in the same category.

→ Alpha over the benchmark — specifically, whether the fund manager is genuinely adding value through investment decisions or simply riding market beta.

→ Consistency ratio showing what percentage of rolling periods the fund has beaten its benchmark, not just whether it has beaten it in the most recent period.

→ Expense ratio compared to the SEBI-mandated TER ceiling for that AUM level, and how it compares to the category average.

→ Current fund manager’s tenure in the specific role, their track record across other mandates they have managed, and the fund house’s overall investment team stability.

→ AUM size relative to the investable universe in the fund’s category, particularly for mid-cap and small-cap oriented schemes.

→ Portfolio overlap analysis if you are investing in multiple funds, to ensure you are getting genuine diversification across the portfolio as a whole.

→ The fund’s behaviour during specific market downturns — how much it fell compared to the benchmark during the March 2020 crash or the 2018 mid-cap selloff — to understand real-world risk.

→ Maximum drawdown — the largest peak-to-trough fall in the fund’s history — so you understand the worst case you might have to live through.

One More Thing Worth Knowing — The Behavioural Risk

Even the best fund, evaluated with the most rigorous process, will not help an investor who panics and redeems when markets fall 30%.

A distributor who only analyses fund metrics is doing half the job. The other half is understanding the investor sitting across from them — their actual risk tolerance (not what they say when markets are high, but what they will feel when their portfolio is down significantly), their investment horizon, their income stability, and what that money is actually for.

A twenty-six-year-old with a stable job and no near-term financial goals can handle a high-volatility small-cap fund. A fifty-four-year-old planning for retirement in six years cannot — even if the small-cap fund has a better Sharpe ratio. Suitability is not just a regulatory requirement. It is the foundation of the entire recommendation.

The best distributors spend as much time understanding their client’s financial life as they spend analysing fund metrics. They build a written investment plan — sometimes called an Investment Policy Statement — that documents the client’s goals, timeline, risk capacity, and the reasoning behind every fund recommended. This document protects both the investor and the distributor. And it keeps the investment process grounded in what actually matters: the investor’s specific goals, not the market’s most recent favourites.

How SubhShanti Wealth Helps You Build Financial Confidence — 5 Ways We Work Differently

At SubhShanti Wealth, we believe that good financial advice is not about recommending the most popular fund or chasing last year’s returns. It is about building a process — one that is grounded in research, aligned with your goals, and honest about the risks involved at every step.

Here are five ways we bring that belief into practice for every client we work with.

1. We Evaluate Funds on Metrics That Actually Matter

Most investors encounter mutual funds through star ratings and point-to-point return charts. At SubhShanti Wealth, we go several layers deeper. Before recommending any scheme, we examine rolling returns across seven to ten years, Sharpe ratios against category peers, alpha generated over the benchmark, consistency ratios across market cycles, and fund manager tenure in the specific role.

This approach filters out funds that looked strong because their sector happened to perform — and surfaces funds that have demonstrated genuine, repeatable outperformance over time. If you would like to understand how we approach this, our detailed guide on how to reduce portfolio overlap in mutual funds explains the method we use. The goal is to recommend schemes you can hold through a full market cycle without second-guessing the original decision.

2. We Build Portfolios Around Your Goals, Not Market Trends

A twenty-eight-year-old saving for a home in five years and a fifty-year-old building retirement income need completely different portfolios — even if both come to us in the same week asking about equity funds.

At SubhShanti Wealth, every client engagement begins with a structured conversation about financial goals, timelines, income stability, and existing obligations. We then build a written investment plan that documents the reasoning behind every allocation. This plan becomes the reference point for every portfolio review, every market correction, and every new fund we consider adding. Portfolios built around goals stay invested. Portfolios built around trends do not.

3. We Talk About Risk Before We Talk About Returns

Risk tolerance is one of the most misunderstood concepts in personal finance. Most investors know their risk tolerance when markets are rising. Very few have actually tested it during a 35% drawdown.

Our approach at SubhShanti Wealth involves an honest, detailed conversation about what downside looks like — in rupees, not percentages — before any investment recommendation is made. This is not a formality. Risk profiling is the foundation on which every portfolio we build sits. Done properly, it changes which funds we recommend, how much equity exposure we suggest, and how we structure the portfolio across time horizons. We have written in detail about why this step matters so much — you can read it here: Your Guide to Risk Profiling: Why Your Mutual Fund Distributor Must Assess You Before Recommending Funds. We walk clients through historical drawdown data, maximum loss scenarios, and realistic recovery timelines for every category of fund we consider. This prepares investors mentally for what markets inevitably bring. Clients who understand the downside before they invest are far less likely to redeem at the worst possible moment.

4. We Are Fully Transparent About How We Work and What We Earn

SubhShanti Wealth is an AMFI-registered Mutual Fund Distributor. We earn a commission from fund houses when clients invest through us in regular plans. We disclose this clearly, in writing, before any transaction is initiated.

We also explain — without being asked — the difference between regular and direct plans, and where each makes sense for a client’s specific situation. Clients who choose to work with us do so knowing exactly what they are paying for and why. That transparency is not a regulatory requirement we grudgingly fulfill. It is the standard we hold ourselves to because we believe long-term client relationships can only be built on complete honesty.

5. We Stay Involved After the Investment Is Made

The investment decision is only the beginning. Markets move. Life circumstances change. Fund managers get replaced. Expense ratios shift. Sectors that drove returns in one cycle become a drag in the next.

At SubhShanti Wealth, every client portfolio receives periodic structured reviews that go beyond checking whether returns are up or down. We revisit the original goals, check whether the portfolio’s risk profile still matches the client’s situation, monitor the funds themselves for changes in management or strategy, and rebalance where necessary. We also stay available between reviews — because the questions that matter most often arise at 11 pm before a major financial decision, not during a scheduled meeting.

Final Thoughts

Star ratings are a convenience. They compress complex information into a simple number that is easy to glance at and easy to act on. There is nothing wrong with noticing that a fund has four or five stars. But a rating should open the conversation, not close it.

The real work of mutual fund selection — for a distributor who takes their responsibility seriously — happens in the rolling return tables, the risk-adjusted metrics, the portfolio construction analysis, and the honest conversation about what the investor can actually live through when markets get difficult.

When you work with a distributor who can walk you through this kind of analysis, you are not just getting someone who processes your paperwork. You are working with someone who understands what they are recommending and why — and who can stand behind that recommendation not just when markets are rising, but when they are not.

That combination of analytical depth and investor-first thinking is what separates a genuinely good mutual fund distributor from the rest.

| Disclaimers Mutual fund investments are subject to market risks. Please read the Scheme Information Document (SID), Statement of Additional Information (SAI), and Key Information Memorandum (KIM) carefully before investing. The NAV of schemes may go up or down depending on market conditions. Past performance may or may not be sustained in the future. This content is prepared for informational and educational purposes and does not constitute investment advice or a solicitation to invest. Investors are advised to consult their financial advisor before making investment decisions. Distributors must ensure all recommendations are suitable to the investor’s risk profile and financial goals as required under AMFI’s Code of Conduct for Mutual Fund Distributors. |